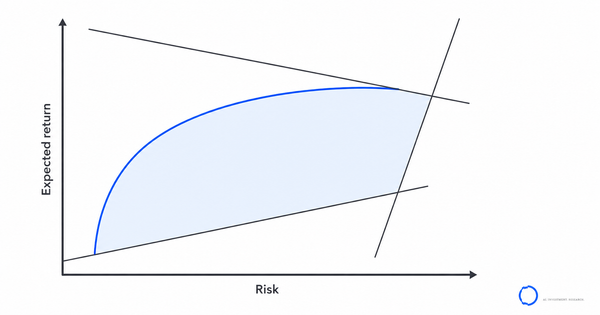

Portfolio optimisation under real-world constraints

A practitioner's guide to portfolio optimisation constraints: turnover, cardinality, transaction costs, estimation error, and three diagnostics to run now.

A practitioner's guide to portfolio optimisation constraints: turnover, cardinality, transaction costs, estimation error, and three diagnostics to run now.

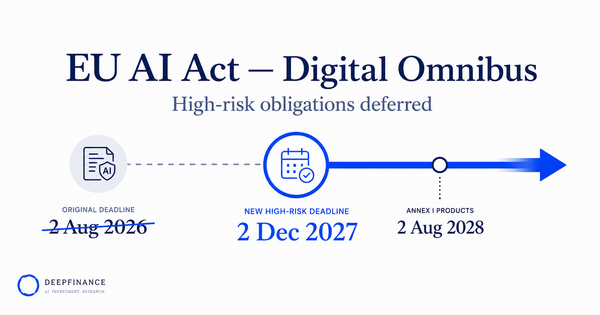

The EU AI Act Digital Omnibus delays high-risk obligations to December 2027 — what stays in force in 2026 and what it means for financial firms.

Aspects Q2 2026 — four risk signatures in Tech & AI infrastructure: capex-financing migration, market concentration, the power constraint, and AI Act governance.

Risk Heartbeat June 2026 — non-bank leverage and private-credit concentration graduates to a flagged signal, the energy-led reflationary regime stays modal through the ECB's 11 June decision, and dollar-funding stress enters the watchlist.

Risk Heartbeat May 2026 — an energy supply shock pushes the reflationary-surprise regime to modal, cross-border payment-system stress graduates to a flagged signal, and non-bank leverage enters the watchlist.

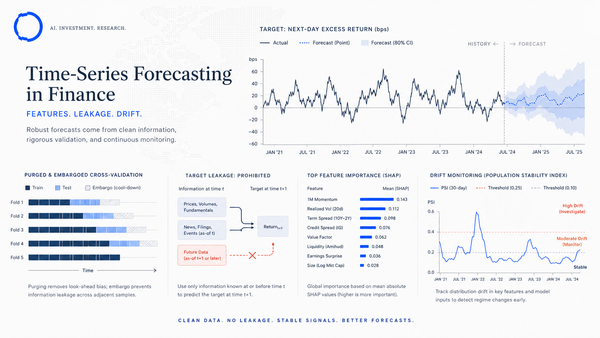

Practitioner's playbook for time-series forecasting in finance — feature engineering, target leakage, drift monitoring, and three diagnostics to run now.

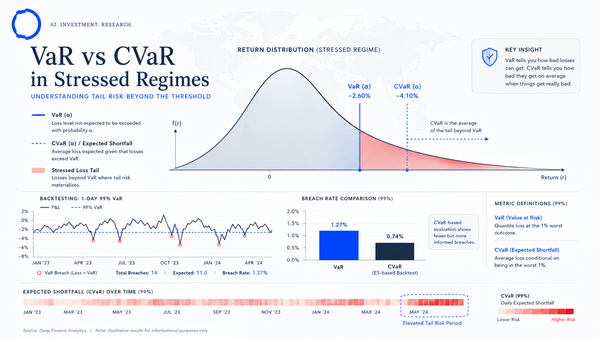

VaR vs. CVaR in stressed regimes — a benchmark on 2008 and 2020 with breach rates, magnitudes, and three notes for running CVaR in production.

Risk Heartbeat April 2026 — commodity-financing dispersion graduates, second-order Financials contagion partially resolves, new payment-system signal.

A free-tier sector risk lens — aggregate idiosyncratic risk, Risk Heartbeat coherence, sentiment compression, microstructure and regulatory signal by sector.

Two-tier AI agents — a cheap triage classifier in front of a deep LLM extractor. Cost, precision, and governance benefits, with the full design pattern.

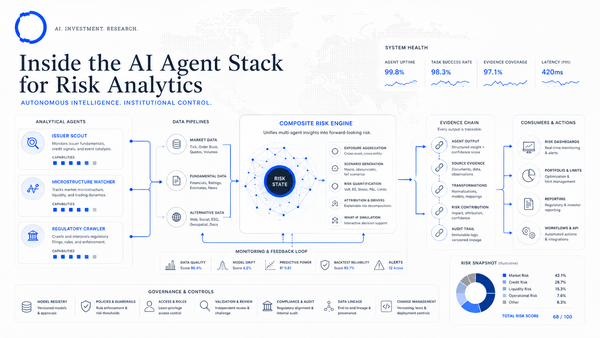

Technical walkthrough of Issuer Scout, Microstructure Watcher, Regulatory Crawler — the AI agent stack architecture behind Risk Heartbeat at DF Analytics.

Risk Heartbeat March 2026 — Financials signal priced in, commodity-financing dispersion graduates, EU AI Act clarifying note on agent documentation.

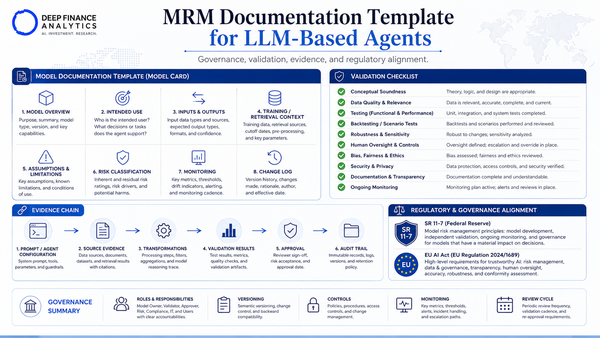

An 11-section MRM documentation template for LLM-based agents — practical, continuous, runtime-generated. Aligned with SR 11-7 and the EU AI Act.

EU AI Act readiness checklist — 30 items across inventory, data, robustness, transparency, documentation, and vendor governance for asset managers in 2026.

ai governance financial services

Nine operational principles for AI governance in financial services — explainability, model registry, challenger models, drift monitoring, audit-readiness.

risk heartbeat february 2026

Welcome to issue #02 of Risk Heartbeat. February is a short month and a busy one — three of the four signals we covered in January moved meaningfully, and one materially new signal entered our watchlist. The format is the same as last month: what changed, three flagged signals, one macro

factor models institutional risk"

Where factor models still earn their place in 2026 and where they hide risk — residual concentration, stale loadings, non-stationary premia, and the fix.

idiosyncratic risk scoring

Epsilon scores idiosyncratic risk for every issuer in the investable universe, daily, using two-of-three coherence across price, narrative, and microstructure.

inancials liquidity stress signatures

Aspects Q1 2026 — four early-warning Financials liquidity stress signatures, the issuer clusters they identify, and the portfolio implications.

risk heartbeat january 2026

Risk Heartbeat January 2026 — three agent-flagged signals on idiosyncratic dispersion, EM sovereign liquidity, EU AI Act enforcement, plus macro lens.

portiq scenario engine

Walk through the PortIQ scenario engine — describe a stress in plain English, see factor shocks, P&L impact, and ranked hedging proposals in seven minutes.

ai-native risk intelligence

Five concrete tests that separate AI-native risk intelligence from legacy risk reporting with an LLM bolted on. A buyer's working definition.

df analytics insights

If you have landed here on day one, welcome. This is the inaugural post on DF Analytics Insights — the editorial home for the research, methods, and product thinking behind everything we build at Deep Finance Analytics.