Aspects Q2 2026: Tech & AI infrastructure

Aspects Q2 2026 — four risk signatures in Tech & AI infrastructure: capex-financing migration, market concentration, the power constraint, and AI Act governance.

This is the second issue of Aspects, the quarterly long-read on the DF Analytics Insights hub. The mandate is unchanged: take one sector or one regime per quarter, look at it through the lens of idiosyncratic risk and our agent stack, and publish something rigorous enough to put on the IC's desk.

Q1 looked at Financials. Q2 turns to Tech & AI infrastructure — the sector that has absorbed more capital, and more index weight, than any other in recent years, and the one whose risk profile is changing fastest. We flagged this pivot at the end of the Q1 Aspects: the dispersion patterns are different here, but the principles transfer.

We are not calling a top. This is a real industry building real capacity for real demand. What this Aspects documents is narrower and, we think, more useful: four signature patterns our agents are flagging across the sector now, how they reinforce one another, and what we would do about them if we were running an institutional book today.

12-minute read · Updated June 2, 2026

Key takeaways

- Four signatures coincide across the Tech & AI infrastructure complex: a migration of capex from cash flow to debt and off-balance-sheet vehicles, index concentration coupling, the power-and-supply constraint becoming the binding limit, and an AI Act governance overhang.

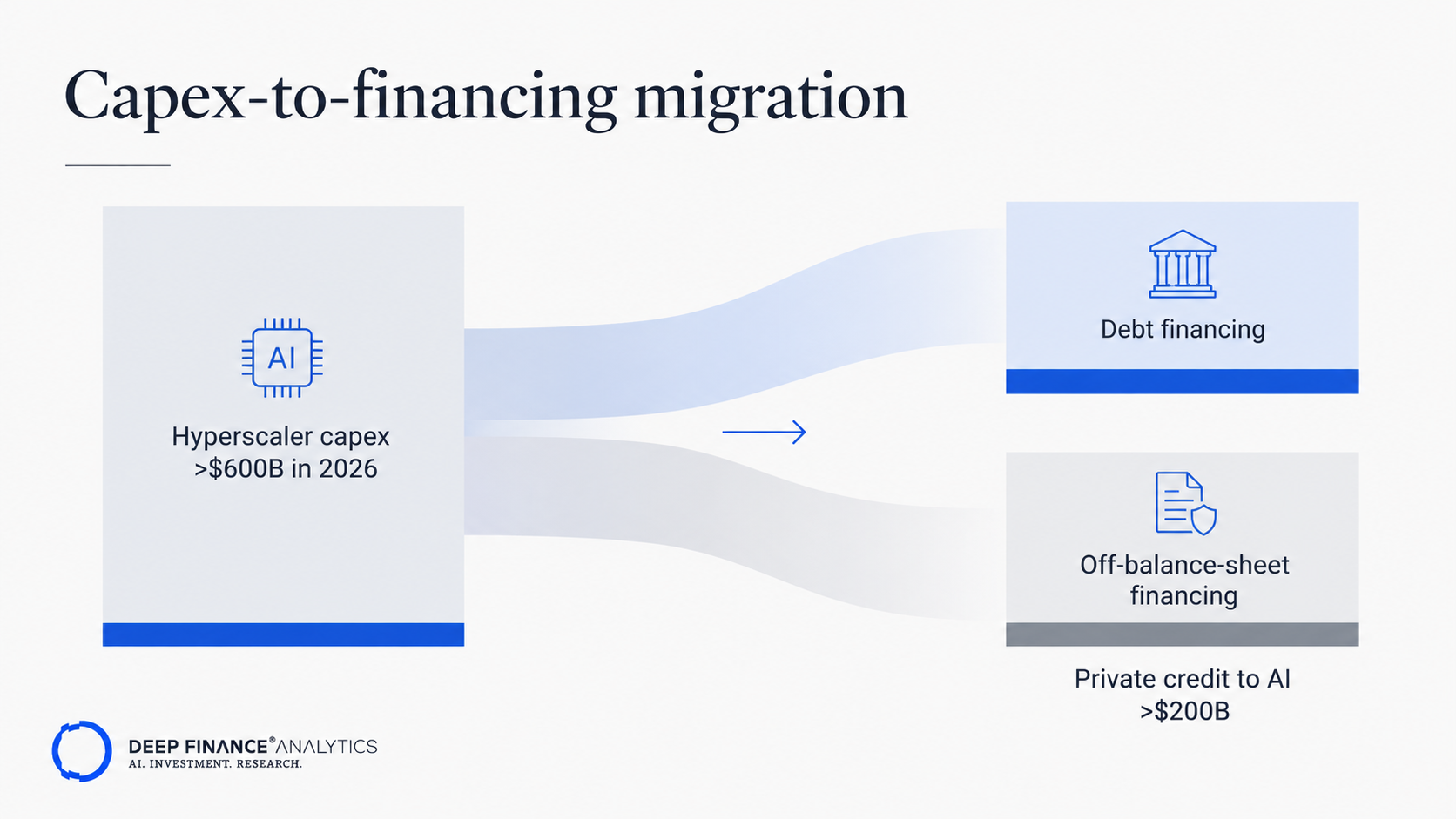

- Hyperscaler capital spending is set to clear $600 billion in 2026, and an increasing share is funded by debt rather than cash flow — including off-balance-sheet structures the BIS describes as "shadow borrowing."

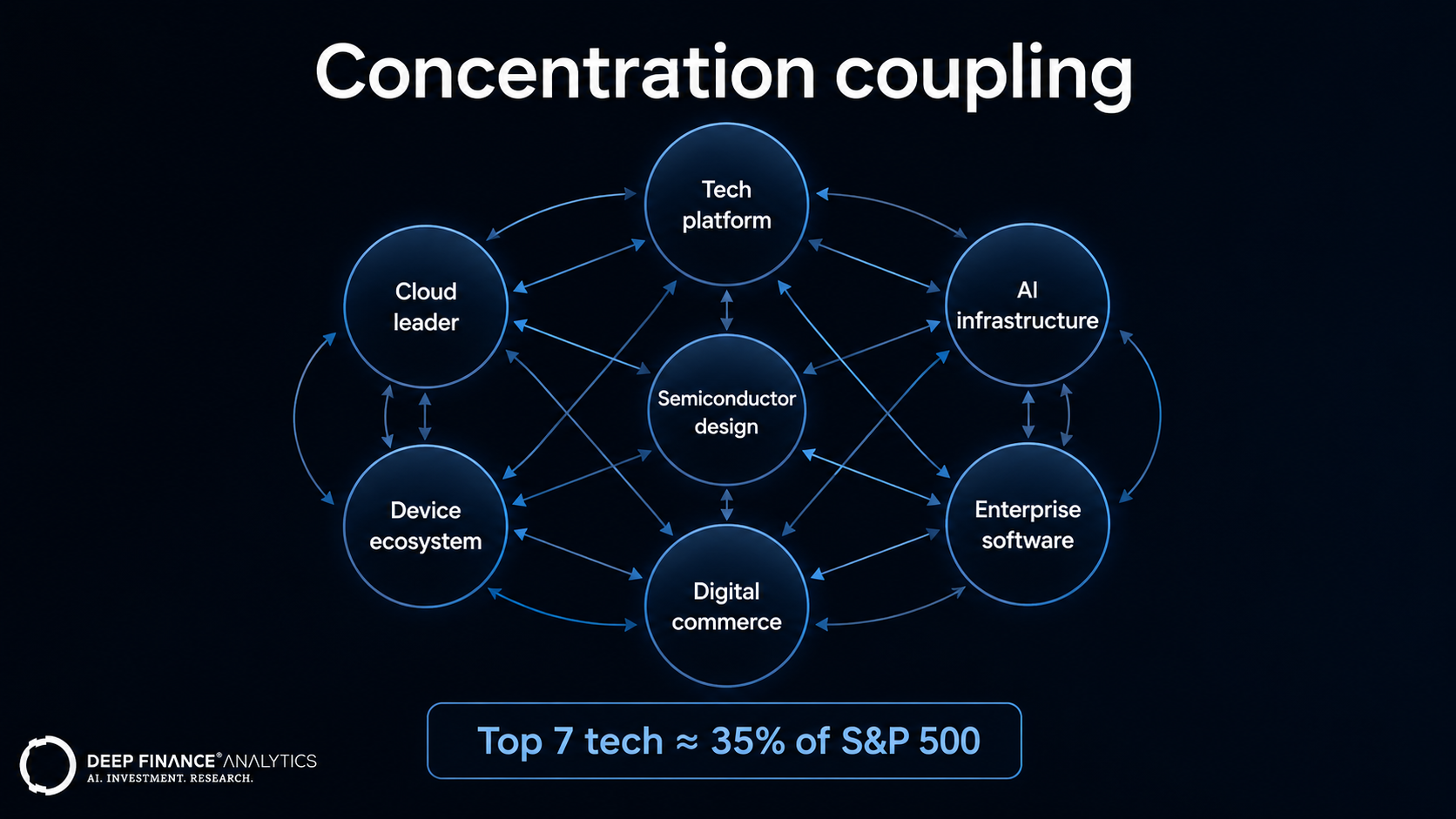

- The largest seven US technology companies now make up roughly 35% of the S&P 500, so a sector-specific shock is no longer a diversifiable event for index-benchmarked books.

- Action: treat AI-infrastructure financing as leverage even when it sits off-balance-sheet, run a concentration look-through to shared customers and counterparties, stress the power constraint, and document AI Act exposure before enforcement begins.

How to read this Aspects

The Aspects format is consistent across issues:

- The sector lens — what is distinct about the sector for AI-native risk analytics.

- The signature patterns — the four (or five, or three) patterns we are flagging.

- The data view — what the numbers show, where we can show them.

- The portfolio implications — what a PM or a CRO might do.

- The watchlist for next quarter — what we will be tracking.

Every Aspects comes with a downloadable PDF for IC distribution. The gated edition names the specific issuers and structures; the public version describes the patterns.

The sector lens — why Tech & AI infrastructure is hard

If Financials are hard to analyse because the balance sheet is opaque, Tech & AI infrastructure is hard for almost the opposite reason: the balance sheets look pristine, and the risk has moved off them.

Three features make this sector distinct for risk analytics:

- The capital intensity is new. A group of companies the market priced as asset-light compounders has, in two years, become one of the most capital-hungry industries on the planet. The risk question is no longer only "what are earnings?" but "how is the build financed, and what happens to that financing in a downturn?"

- The concentration is structural. The same handful of names are at once the largest index weights, the largest capex spenders, and each other's largest customers and suppliers. Revenue, capacity, and valuation are coupled across a small set of issuers — idiosyncratic risk hiding inside what looks like a diversified index.

- The binding constraint is physical. For the first time, the limit on growth is not chips or code but megawatts, grid interconnection, and supply chains. Physical constraints fail differently from financial ones: slower to build, harder to reverse once they bind.

The analytic implication runs through every Aspects: factor models and time-series anomaly detection catch only a fraction of what matters. The decisive signal sits in the unstructured and structural layers — financing structures, customer-concentration disclosures, power agreements, regulatory filings — and in the coherence across them.

The four signatures we are watching

Signature 1 — Capex-to-financing migration

What we look at: How the AI-infrastructure build is being paid for, and where the resulting obligations sit. Issuer Scout aggregates capex guidance, debt issuance, joint-venture and special-purpose-vehicle structures, and lease commitments from filings, transcripts, and primary debt documentation.

What we are seeing: A clear migration from cash-funded to debt-funded and off-balance-sheet capacity. Hyperscaler capital spending is on track to exceed $600 billion in 2026, and a growing portion is no longer self-funded from operating cash flow. Private-credit lending to AI-related borrowers has grown from near-zero to more than $200 billion in a few years, and an increasing share of the build runs through dedicated vehicles — joint ventures and SPVs that raise debt against data-centre assets while the operator holds a minority stake plus a long-term lease or offtake. The BIS calls the resulting obligations "shadow borrowing": economically akin to debt, but largely off the corporate balance sheet.

Why it matters: This is the same channel we flagged from the supervisory side in Risk Heartbeat #06 — leveraged non-banks holding concentrated, richly-valued assets — viewed from the sector that is now its largest single growth area. A pristine balance sheet that has quietly term-financed its buildout off-sheet is more fragile than it screens, and that fragility surfaces exactly when refinancing tightens.

Operationalised: Treat off-balance-sheet AI financing as leverage in your stress framework, not as operating expense. For issuers in the high-migration cluster, map lease and offtake commitments and SPV debt maturities alongside the on-balance-sheet picture before trusting the headline net-cash position.

Signature 2 — Concentration coupling

What we look at: The degree to which index weight, capex, revenue, and counterparty exposure concentrate in the same small set of names. Risk Brain and our factor view decompose how much of an index-benchmarked book's risk is genuinely idiosyncratic versus a single coupled bet.

What we are seeing: Concentration has reached a level that changes the risk arithmetic. The largest seven US technology companies now account for roughly 35% of the S&P 500, and the ten largest names sit close to 40%. More telling than the level is the coupling: the same issuers are each other's customers and suppliers, so a slowdown in one firm's AI spending is a revenue event for the next. Variance that looks diversified at the index level is, on a look-through, a concentrated bet on a single theme.

Why it matters: When a sector this large is also this interconnected, a sector-specific shock stops being diversifiable for benchmarked portfolios. The circular revenue relationships — chips sold to clouds, capacity sold to model labs, compute resold to enterprises — mean first-round and second-round shocks land on overlapping names.

Operationalised: Run a concentration look-through that nets exposure across shared customers, suppliers, and counterparties rather than treating each ticker as independent. Epsilon users can isolate the idiosyncratic component of each name and see how much of the "diversified" book is one coupled AI-capex factor.

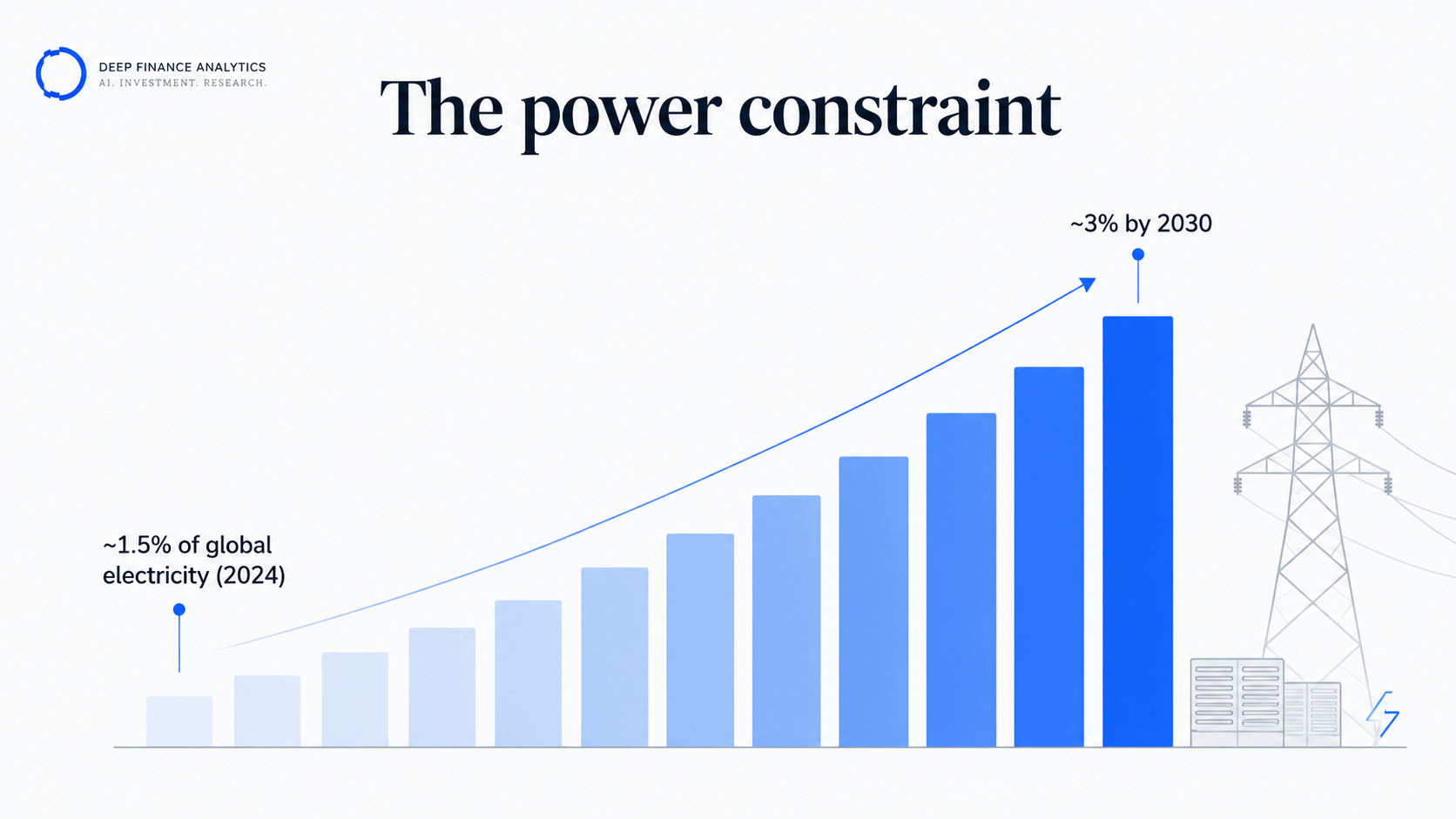

Signature 3 — The power and supply constraint

What we look at: The physical limits on the build — electricity, grid interconnection, cooling, and the equipment supply chain — and the gap between announced capacity and deliverable capacity. Our agents read power-purchase agreements, interconnection-queue disclosures, utility filings, and supplier commentary.

What we are seeing: The binding constraint is shifting from silicon to power. Data centres consumed roughly 1.5% of global electricity in 2024, a share the IEA expects to roughly double by 2030 toward about 3%, with AI the dominant driver and electricity demand from accelerated servers growing at double-digit annual rates. Against that, grid interconnection and power availability are not keeping pace with announced buildout. The dispersion we flag is between operators with secured, contracted power and those whose announced capacity depends on infrastructure that does not yet exist.

Why it matters: Physical constraints introduce a delivery risk that markets are not used to pricing in technology names. Announced capacity that cannot be powered on schedule becomes stranded capital and missed offtake — and, where it was debt-financed, a financing problem. The constraint also concentrates pricing power in whoever controls scarce power and interconnection.

Operationalised: For names whose growth case rests on capacity additions, discount announced capacity to contracted, powerable capacity. Flag any issuer whose financing assumes a buildout faster than its secured power supply realistically allows.

Signature 4 — The AI Act governance overhang

What we look at: Regulatory Crawler's stream of AI-specific regulation, guidance, and enforcement signals — the EU AI Act first, but also the wider supervisory direction on AI in finance from the BIS, the FSB, and national regulators.

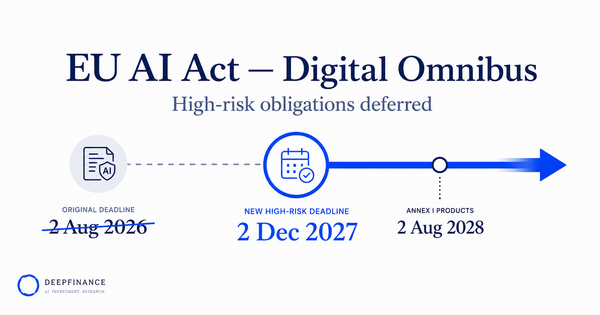

What we are seeing: The regulatory perimeter is hardening on a known timetable. Under the EU AI Act, obligations for general-purpose AI models have applied since August 2025, the AI Office's enforcement powers arrive in August 2026, and the high-risk obligations for Annex III systems are now subject to a proposed deferral to December 2027 under the Digital Omnibus. The direction is unambiguous even where exact dates move: documentation, conformity assessment, and accountability are becoming binding, with penalties scaled to global turnover.

Why it matters: For the model and infrastructure providers at the centre of this sector, governance is moving from reputational to enforceable. For the institutions deploying their tools — including in finance — the burden lands on the deployer as well as the provider. A mostly-known timetable is exactly the kind of risk to price and prepare for in advance, not discover at enforcement.

Operationalised: Inventory where AI systems sit in your stack, classify them against the AI Act's risk tiers, and document the governance now — the discipline we set out in our EU AI Act readiness work. For exposure to provider names, treat the regulatory timetable as a scheduled risk event, not a tail.

The data view

Where we can publish numerical comparisons in this public Aspects, we do. The gated edition contains the issuer-level appendix. Selected figures, each from a credible external source and verified this quarter:

- Hyperscaler capital spending: on track to exceed $600 billion in 2026, with an increasing share funded by debt rather than operating cash flow.

- Private-credit lending to AI-related borrowers: from near-zero to more than $200 billion in a few years, much of it through off-balance-sheet vehicles.

- US technology concentration: the largest seven names ≈ 35% of the S&P 500; the largest ten ≈ 40%.

- Data-centre electricity: ≈ 1.5% of global consumption in 2024, projected by the IEA to roughly double by 2030 toward ~3%, AI the dominant driver.

We do not read any single one of these as a forecast. The point of Aspects is the coherence: financing migration, concentration coupling, a physical constraint, and a regulatory timetable, all pointing the same way, in the same sector, at the same time.

Portfolio implications

For a portfolio with material Tech & AI infrastructure exposure — which, given the concentration, is most index-benchmarked portfolios — four adjustments follow from the data:

- Treat off-balance-sheet AI financing as leverage. Bring SPV debt, joint-venture obligations, and long-dated capacity leases into the stress framework; a net-cash headline that excludes shadow borrowing understates refinancing sensitivity.

- Stress concentration on a look-through basis. Net exposure across the shared customers, suppliers, and counterparties that couple these names, then size the idiosyncratic residual. PortIQ users can run an AI-capex-slowdown scenario that propagates through the circular revenue relationships rather than hitting one name in isolation.

- Discount announced capacity to powerable capacity. Where a growth case or a financing rests on capacity additions, haircut for secured power and realistic interconnection timelines.

- Document AI Act exposure before enforcement. Classify your AI systems against the risk tiers and keep the governance on file. The answer to "what were you running, and how was it controlled" cannot be assembled retroactively.

What we will be watching in Q3

Four items move onto the Q3 Aspects watchlist:

- Whether capex migration into debt and off-balance-sheet vehicles continues, or reverses on-sheet as scrutiny rises.

- Whether index concentration widens or mean-reverts, and whether the circular revenue relationships decouple.

- Whether the power constraint binds — slipped capacity timelines, stranded debt-financed assets — rather than merely being discussed.

- Whether AI Act enforcement begins on schedule from August 2026, and whether the high-risk deferral to December 2027 holds.

Q3 Aspects will revisit Tech & AI infrastructure if any of these graduate, and otherwise pivot to the next sector where the idiosyncratic-risk lens earns its keep.

How to access the gated edition

The public Aspects covers the patterns and the methodology. The gated edition adds the issuer-level appendix with named entities and financing structures, the concentration look-through methodology and composite signal definitions, a worked PortIQ AI-capex-slowdown scenario, and a one-page IC summary. It is available on request to qualifying institutional readers.

Frequently asked questions

What is the Q2 2026 Aspects about?

It is the quarterly DF Analytics long-read on Tech & AI infrastructure. It documents four risk signatures — capex-to-financing migration, concentration coupling, the power-and-supply constraint, and the AI Act governance overhang — and how they reinforce one another across the sector.

Why is off-balance-sheet AI financing a risk if the companies hold net cash?

Because the economic obligation persists even when the accounting does not show it on the corporate balance sheet. Hyperscalers increasingly fund capacity through joint ventures and SPVs that raise debt against the assets, with the operator holding a minority stake plus long-term lease or offtake commitments — what the BIS calls "shadow borrowing." A net-cash headline that excludes it understates refinancing sensitivity.

Why does technology market concentration matter for a diversified portfolio?

Because at roughly 35% of the S&P 500 in the largest seven names, a sector-specific shock is no longer diversifiable for an index-benchmarked book. The concentration is also coupled — the same issuers are each other's customers and suppliers — so first- and second-round shocks land on overlapping names. On a look-through, much of the "diversified" exposure is a single AI-capex bet.

What changes under the EU AI Act in 2026?

Obligations for general-purpose AI models have applied since August 2025, and the AI Office's enforcement powers arrive in August 2026. High-risk obligations for Annex III systems are now subject to a proposed deferral to December 2027 under the Digital Omnibus. Documentation, conformity assessment, and accountability become binding, with penalties scaled to global turnover.

How does this Aspects relate to the June Risk Heartbeat?

Two angles on one vulnerability. Risk Heartbeat #06 flagged non-bank leverage and private-credit concentration from the supervisory side; this Aspects shows Tech & AI infrastructure is now the largest single destination for that financing, and traces the sector-level signatures that result.

Related reading

- Aspects Q1 2026: Financials liquidity signatures

- Risk Heartbeat #05 — May 2026 issue

- Industry Risk Intelligence Platform — free sector lens

External references

- BIS — Financing the AI infrastructure boom: on- and off-balance-sheet borrowing

- IEA — Energy and AI: energy demand from AI

- European Commission — AI Act regulatory framework

About the author — Research team — Deep Finance Analytics. Our Research team produces the agent-driven signal and quantitative analysis behind Risk Heartbeat and Aspects. See the Insights hub for the full archive, or book a discovery call to discuss this post with the team.