Risk Heartbeat #05 — May 2026 issue

Risk Heartbeat May 2026 — an energy supply shock pushes the reflationary-surprise regime to modal, cross-border payment-system stress graduates to a flagged signal, and non-bank leverage enters the watchlist.

Welcome to issue #05 of Risk Heartbeat. May was the month the macro backdrop stopped being benign. A geoeconomic energy shock — the Middle East conflict and the oil-price spike it triggered — pushed inflation back up on both sides of the Atlantic, and for the first time in 2026 the reflationary-surprise regime became the modal state in our macro book.

It was also the month a watchlist signal we shared early actually matured, which is the discipline this series exists to demonstrate. The format is unchanged: what changed, three flagged signals, one macro lens, reader question, what we are reading.

9-minute read · Updated May 26, 2026

Key takeaways

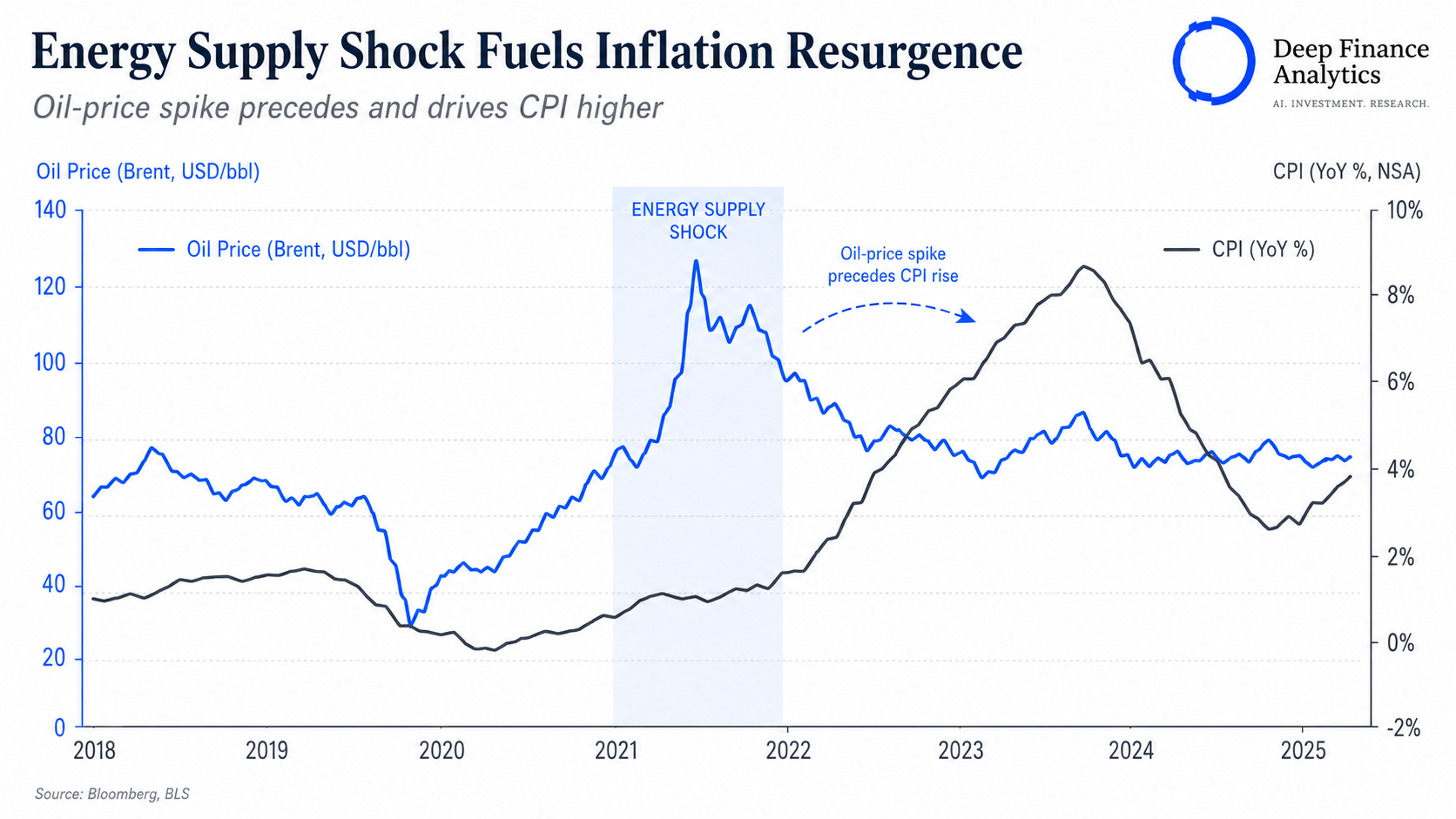

- An energy supply shock drove a genuine inflation resurgence: US headline CPI jumped to 3.8% in April (energy +17.9%), core held at 2.8%, and the Fed stayed on hold amid the most dissents since 1992; euro-area inflation expectations were revised up and markets moved to price an ECB hike.

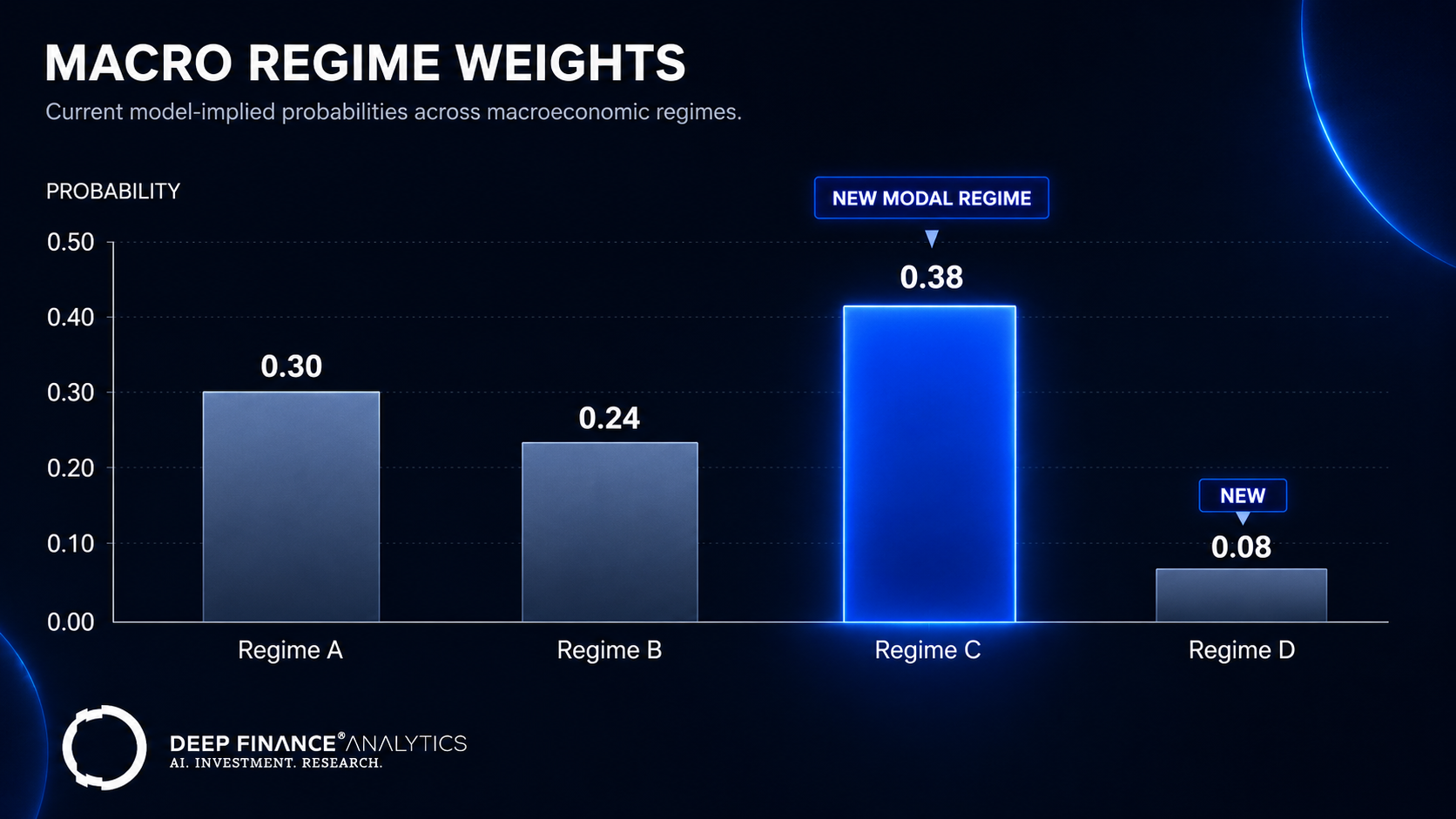

- Regime C ("reflationary surprise") became modal at 0.38; the compressed-vol Regime A fell sharply to 0.30 as a real shock displaced the benign state.

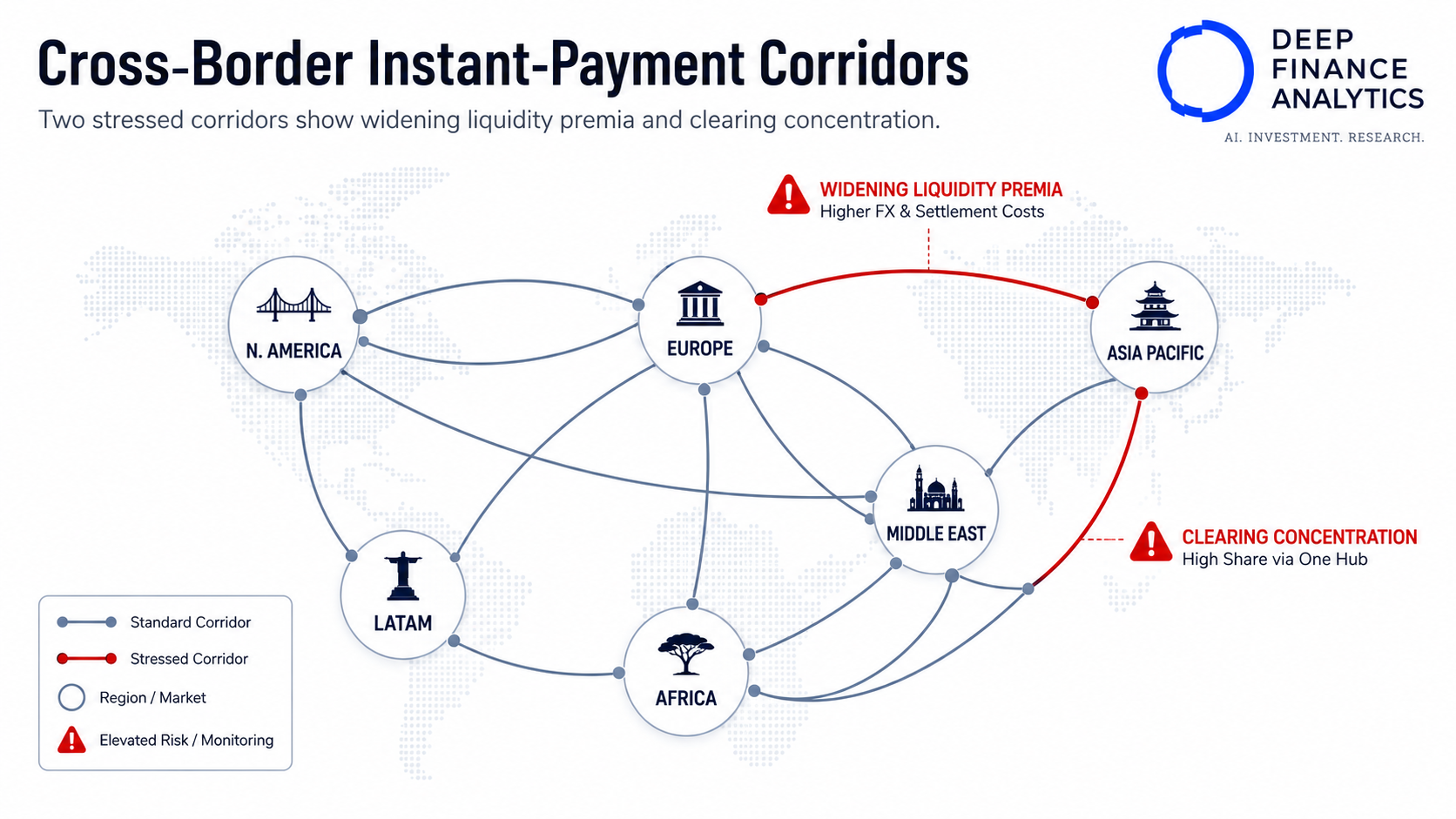

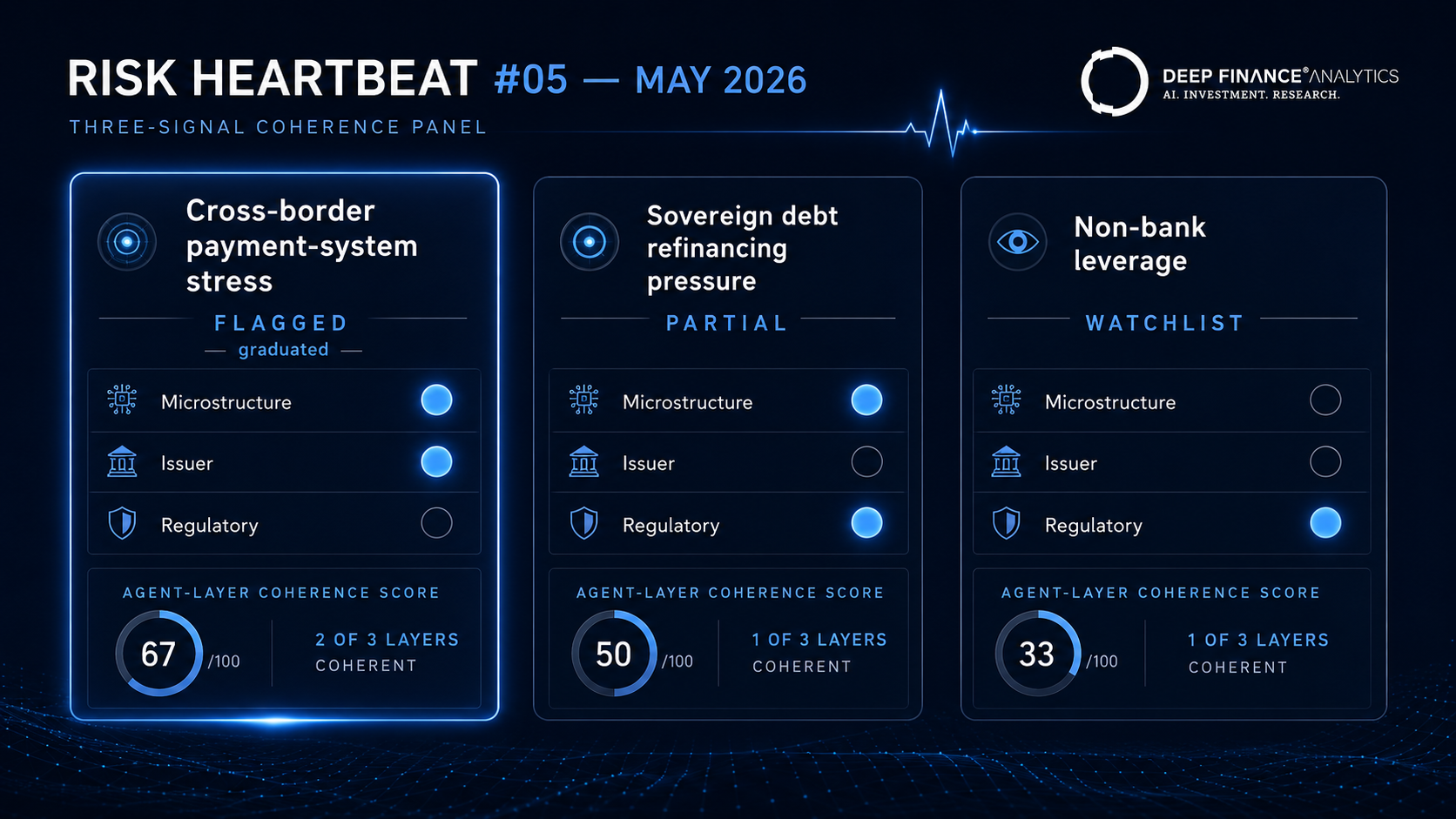

- Cross-border payment-system stress, flagged to the watchlist in April, graduated to a fully flagged signal and triggered the addition of Regime D ("plumbing stress").

- A new watchlist entry — non-bank leverage and concentrated US-asset valuations — opened on the back of the ECB's May Financial Stability Review.

What changed in May 2026

Three headlines:

- An energy shock turned the macro book. The escalation in the Middle East and the associated oil-price spike fed straight into the data: US headline inflation accelerated to 3.8% — its highest since May 2023 — with energy up 17.9% year-on-year. This is no longer a forecast risk; it is a realised supply shock, and it re-weighted the entire macro lens.

- Cross-border payment-system stress graduated. The watchlist entry we opened in April reached two-of-three coherence this month when Regulatory Crawler began picking up supervisory communications in one of the two affected corridors. It is now a fully flagged signal and the trigger for adding Regime D to the macro book.

- Non-bank leverage entered the watchlist. Following the ECB's May Financial Stability Review — which flagged elevated non-bank liquidity and leverage vulnerabilities alongside concentrated holdings of richly-valued US assets — Issuer Scout and Microstructure Watcher began aligning on a dispersion signal in leveraged non-bank intermediaries. It is early; we are sharing it now, as we always do.

Three flagged signals

Signal #1 — Cross-border payment-system stress: graduated to flagged

What the agent flagged: The April watchlist entry — widening intra-day liquidity premia and clearing-institution concentration in two cross-border instant-payment corridors — gained a second coherence layer in May. Regulatory Crawler detected a cluster of supervisory communications referencing operational and liquidity resilience in one of the two corridors, lifting the signal from one-of-three to two-of-three coherence and across our publication threshold.

Why it matters: This is the maturation we flagged as uncertain last month. Payment-system stress is rare but consequential because it sits upstream of almost everything else: if a clearing dependency seizes, the loss is operational before it is ever a market loss. The signal remains concentrated in two corridors, and Issuer Scout still shows nothing on the payment names — so this is a plumbing signal, not yet a credit signal.

Operationalised: For institutions with material dependence on clearing counterparties in the affected corridors, the question we posed in April is now a documentation requirement, not a courtesy: map the dependency, name the backup, and rehearse the failover. PortIQ users can run the corridor-outage scenario we published to the scenario library this week against treasury and settlement exposures.

Signal #2 — Commodity-financing dispersion: partial resolution, energy re-test

What the agent flagged: Two of the eight names in the commodity-financing cluster resolved early in May — one through a capital raise that re-priced its bank-capital instruments back toward the cohort, one through an explicit supervisory remediation dialogue picked up by Regulatory Crawler. Then the oil-price spike arrived, and the surviving five names are now being re-tested by exactly the variable their books are most sensitive to.

Why it matters: An energy shock is double-edged for commodity financiers — higher throughput revenue, but higher margin calls, larger drawn facilities, and fatter funding needs. The dispersion signal on the five live names, which had been compressing, stopped compressing in the back half of May. We read that as the shock arresting an in-progress resolution rather than reversing it, but it keeps the cohort firmly on watch.

Operationalised: For exposures in the two resolved names, the cautious overlay can be lifted, with the capital-raise name flagged for follow-through on use of proceeds. For the five live names, hold the overlay and add an explicit oil-price sensitivity to the next re-test.

Signal #3 — Non-bank leverage and US-asset concentration: entering watchlist

What the agent flagged: The ECB's May Financial Stability Review put non-bank financial intermediation back at the centre of the risk conversation, citing persistent liquidity and leverage vulnerabilities and concentrated non-bank holdings of US assets at elevated valuations. In the days after publication, our agents began aligning on a related dispersion: Issuer Scout flagged a cluster of leveraged non-bank intermediaries, and Microstructure Watcher saw funding-sensitivity widen in the same names.

Why it matters: This is the channel through which a market repricing becomes a forced-selling event. If leveraged non-banks holding richly-valued US assets are pushed to deleverage into a falling market — precisely the scenario the ECB describes — the losses propagate back to banks through their financing linkages. It is early and the cross-asset coherence is incomplete, but in a freshly reflationary regime it is exactly the signal worth opening before, not after, it matures.

Operationalised: For institutions with financing or counterparty exposure to leveraged non-banks, this is the month to re-confirm collateral terms and to stress the second-round effect of a US-asset drawdown on those counterparties — not just the first-round mark on your own book.

Macro lens — the Macro Simulator's May read

End-May regime weights:

- Regime A — "Compressed vol, dispersing fundamentals": weight 0.30 (down sharply from 0.40). The benign state lost weight fast once a real supply shock materialised; this is the largest single-month move in the regime this year.

- Regime B — "Coordinated repricing": weight 0.24 (up from 0.20). A common, cross-border shock is the textbook condition for correlated repricing, and the weight reflects it.

- Regime C — "Reflationary surprise": weight 0.38 (up from 0.32) and now the modal regime. The energy-led inflation acceleration is no longer one-sided: US CPI at 3.8% with core sticky at 2.8%, the Fed on hold against the most dissents since 1992, euro-area inflation expectations revised up, and markets moving to price an ECB hike on 11 June. That is a coordinated reflationary surprise, which is exactly what the regime is built to represent.

- Regime D — "Plumbing stress": weight 0.08 (new). Created this month on the back of the graduated payment-system signal, as promised in April. The weight is deliberately small — a single flagged signal in two corridors is not a systemic plumbing regime — but it is now explicit and tracked.

The composite read has flipped from "benign with idiosyncratic stories" to "supply-shocked with correlated risk." The ECB's May Financial Stability Review framed the same backdrop as elevated vulnerability under geoeconomic stress, with non-bank leverage as the propagation channel. Our portfolio discipline this month is the inverse of last month's: where we had been trimming reflation hedges, we are re-staging them, and we are explicitly stressing the second-round non-bank channel rather than only first-round market marks.

Reader question of the month

"You moved the reflationary-surprise regime to modal off one inflation print and a geopolitical event. How do you avoid whipsawing the book if the oil spike reverses next month?" — Head of Macro at a sovereign allocator

A fair challenge, and the honest answer is that we accept some whipsaw risk as the price of being responsive. Two things contain it. First, the regime weights are probabilities, not switches: moving Regime C to 0.38 raises its influence on construction without betting the book on it, and Regime A still carries 0.30. Second, we require the move to be corroborated, not just dramatic — the print mattered because it was confirmed by the policy reaction (Fed dissents, repricing of the ECB path) and by our own cross-asset agents, not because a single number was alarming.

If the oil spike reverses and the policy reaction unwinds, Regime C comes back down as readily as it went up, and we will say so here. The discipline is symmetry: a regime that rises on corroborated evidence falls on corroborated evidence, and we publish both directions.

What we are reading

- The ECB Financial Stability Review, May 2026 — the central document for this month's macro lens, particularly its treatment of non-bank leverage and concentrated US-asset valuations as propagation channels under geoeconomic stress.

- The FSB Non-Bank Financial Intermediation Monitor 2026 — essential context for the new watchlist entry and the second-round channel it describes.

- The forthcoming BIS Quarterly Review — for its recurring work on energy-shock pass-through and cross-border funding.

Coming in June

- 9 June — Backtesting agent signals: how we measure a watchlist hit rate without fooling ourselves.

- 16 June — Energy-shock pass-through: a PortIQ walkthrough on commodity-sensitive books.

- 23 June — Aspects mid-year: the half-time read on the 2026 risk book.

- 30 June — Risk Heartbeat #06.

— The DF Analytics Research team

Frequently asked questions

What does it mean that the payment-system signal "graduated"?

It moved from the watchlist to a fully flagged signal. We require two-of-three coherence across our agent layers — microstructure, issuer, and regulatory — before publishing a signal as flagged. The April entry had only the microstructure layer; in May the regulatory layer appeared in one corridor, crossing the threshold.

Why did the reflationary-surprise regime become modal?

Because a forecast risk became a realised shock. The Middle East conflict and the oil-price spike pushed US headline CPI to 3.8% in April (energy up 17.9%), with core sticky at 2.8%; the Fed held against the most dissents since 1992, and euro-area inflation expectations were revised up with markets pricing a June ECB hike. A coordinated, energy-led inflation surprise is precisely the state Regime C represents.

What is Regime D and why add it mid-year?

Regime D is "plumbing stress" — a state in which operational and liquidity seizure in payment or clearing infrastructure drives risk, independent of market direction. It was added because the graduated payment-system signal describes a world the existing market-state regimes (A–C) cannot represent. Its weight is small (0.08) and removable.

Why open a non-bank-leverage watchlist now?

Because the ECB's May Financial Stability Review explicitly flagged elevated non-bank liquidity and leverage vulnerabilities and concentrated holdings of richly-valued US assets — and our own agents began aligning on a related dispersion in leveraged intermediaries. In a reflationary regime, that combination is the classic precondition for forced deleveraging that spills back to banks.

How do you avoid whipsawing the macro book on a single shock?

By treating regime weights as corroborated probabilities rather than switches. A regime moves only when a data surprise is confirmed by the policy reaction and by our cross-asset agents, it moves at the margin rather than wholesale, and it falls as readily as it rises when the evidence reverses.

Related reading

- Risk Heartbeat #04 — April 2026 issue

- VaR vs. CVaR in stressed regimes: a 2008/2020 benchmark

- Time-series forecasting in finance: features, leakage, drift

External references

- ECB — Financial Stability Review, May 2026

- FSB — Non-Bank Financial Intermediation Monitor 2026

- BIS — Quarterly Review

About the author — Research team — Deep Finance Analytics. Our Research team produces the agent-driven signal and quantitative analysis behind Risk Heartbeat and Aspects. See the Insights hub for the full archive, or book a discovery call to discuss this post with the team.