Risk Heartbeat #06 — June 2026 issue

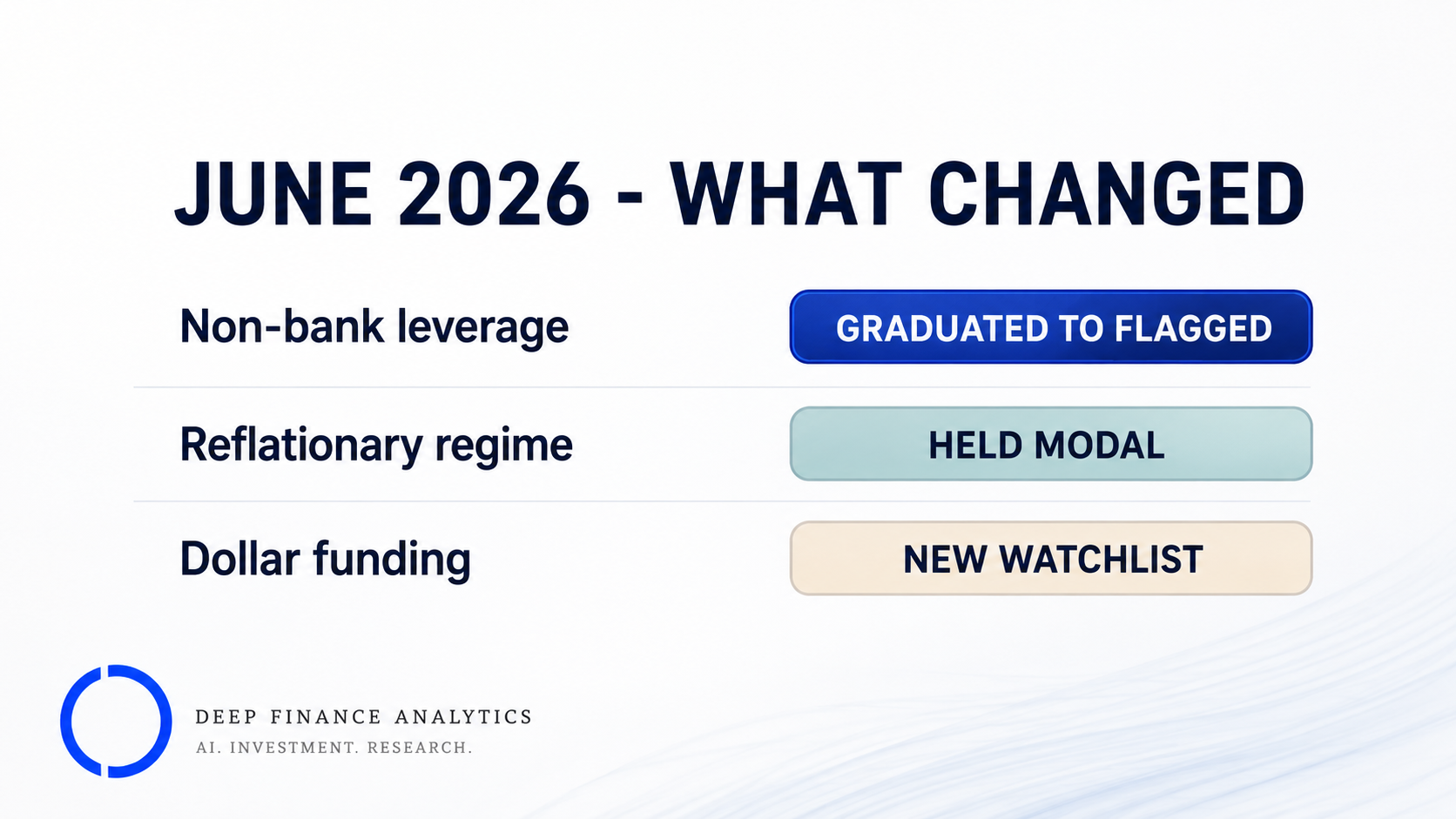

Risk Heartbeat June 2026 — non-bank leverage and private-credit concentration graduates to a flagged signal, the energy-led reflationary regime stays modal through the ECB's 11 June decision, and dollar-funding stress enters the watchlist.

Welcome to issue #06 of Risk Heartbeat. June was the month the macro story stopped being about a single shock and started being about its plumbing. The energy-led reflation that turned the book in May did not reverse — oil held near its highest levels in four years as the Middle East conflict and Strait of Hormuz disruption persisted — and the central question moved from "is inflation back?" to "where does a higher-for-longer rate path break something?"

It was also the month our highest-conviction watchlist entry matured. The non-bank-leverage signal we opened in May gained a second coherence layer and graduated to a fully flagged signal, corroborated by the FSB's own warning on private-credit vulnerabilities. The format is unchanged: what changed, three flagged signals, one macro lens, reader question, what we are reading.

9-minute read · Updated June 30, 2026

Key takeaways

- Non-bank leverage and private-credit concentration — opened to the watchlist in May — graduated to a fully flagged signal in June, corroborated by the FSB's report on private-credit vulnerabilities and its finding that non-banks now hold roughly half of global financial assets.

- The energy-led reflationary regime stayed modal through the ECB's 11 June Governing Council meeting; the decision confirmed that policy is now reacting to a realised inflation shock rather than a forecast one.

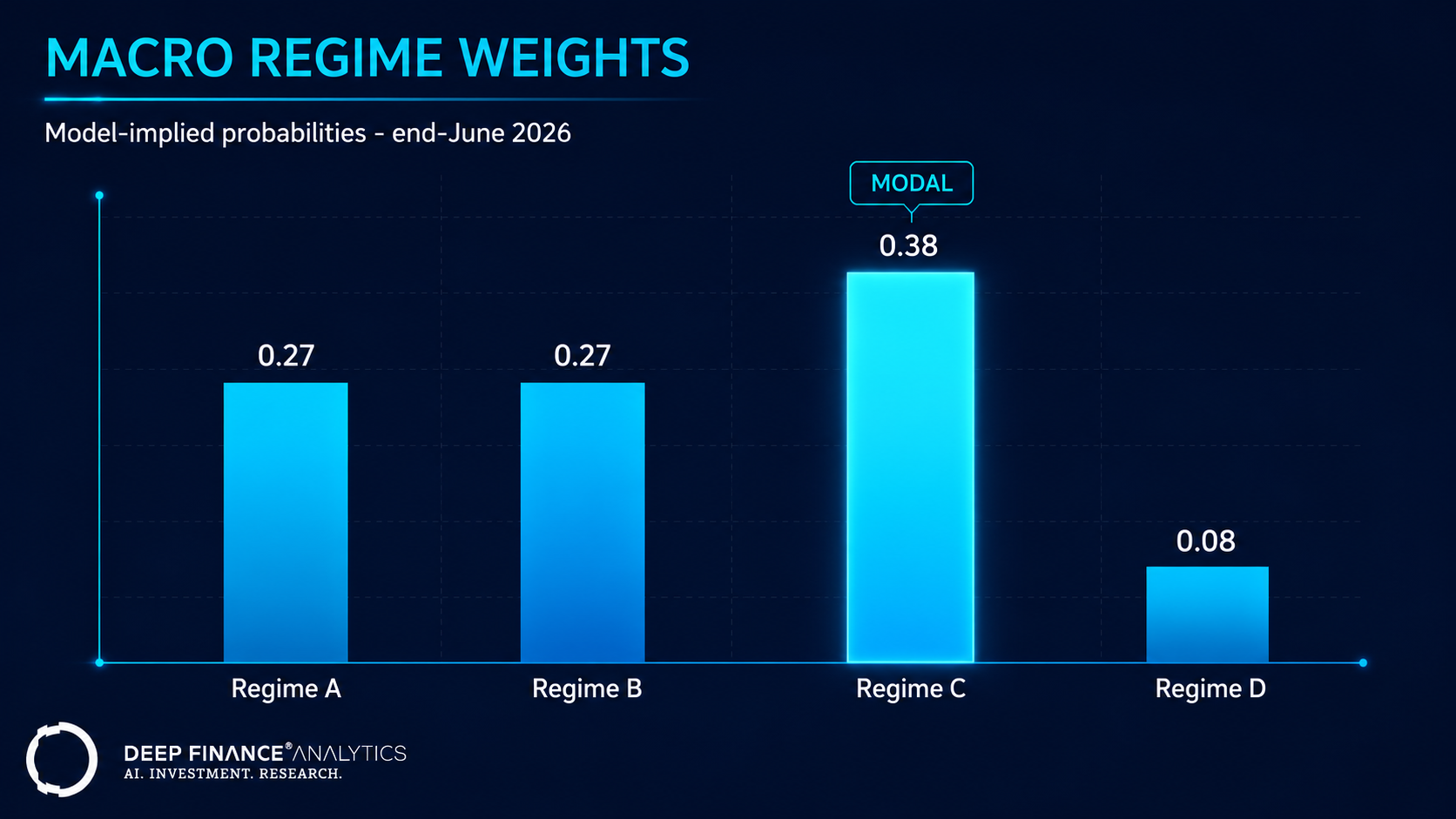

- Regime C ("reflationary surprise") held at 0.38 and remains modal; Regime B ("coordinated repricing") rose to 0.27 as the non-bank deleveraging channel became the dominant propagation risk; the benign Regime A slipped to 0.27.

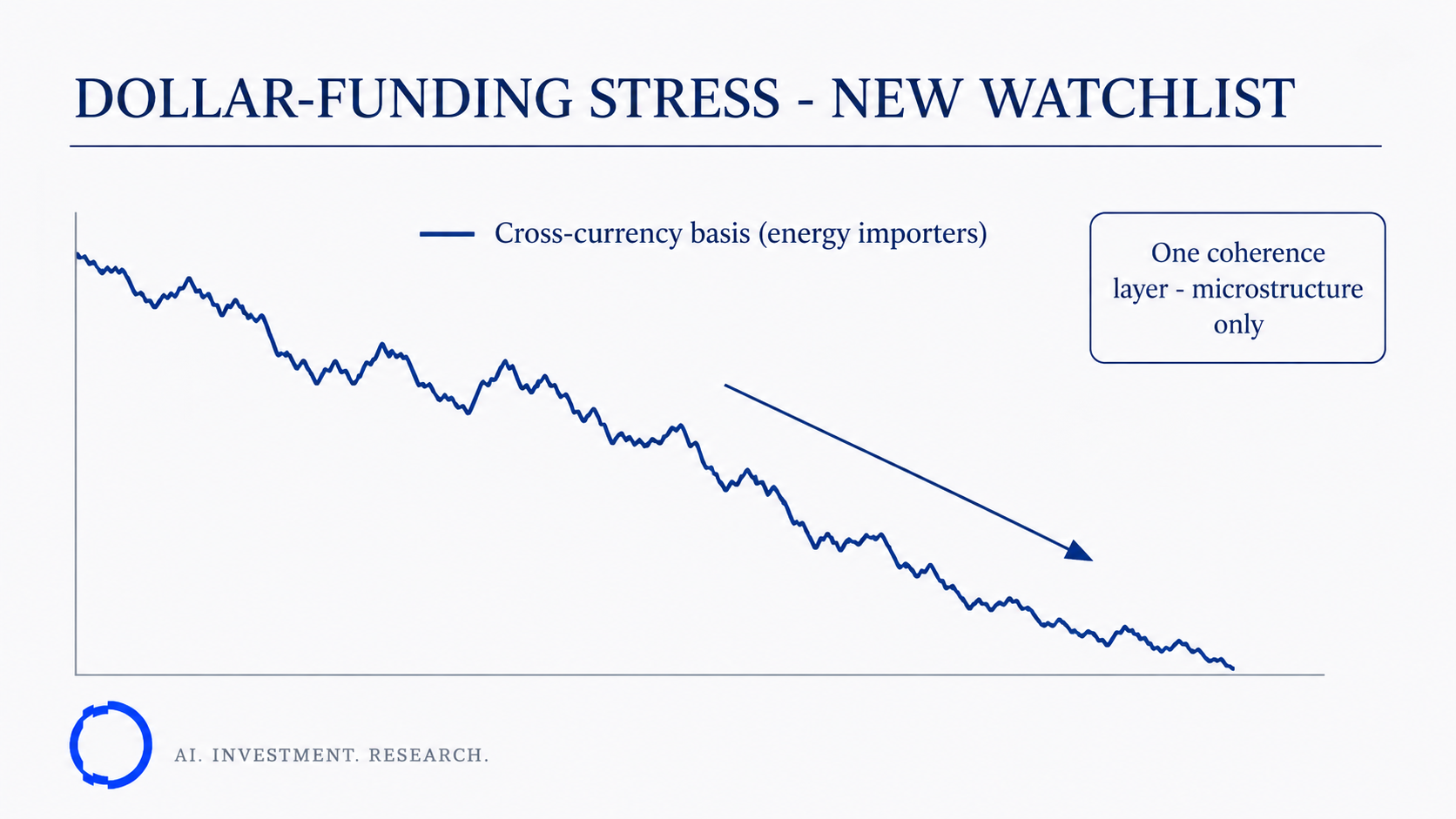

- A new watchlist entry — dollar-funding and cross-currency-basis stress in energy-importing corporates — opened as the energy shock and a diverging policy path pulled on short-dollar balance sheets.

What changed in June 2026

Three headlines:

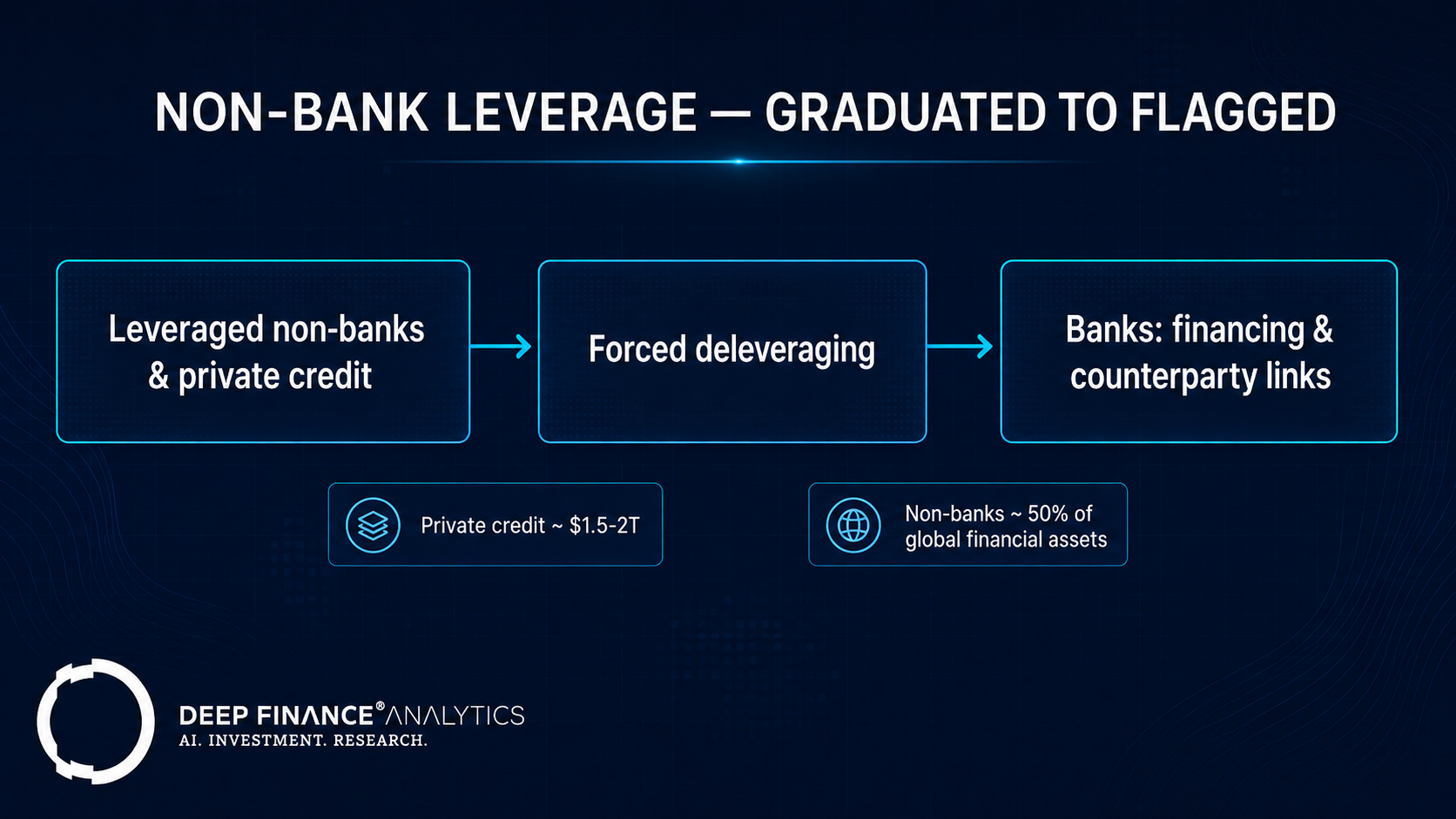

- Non-bank leverage graduated. The watchlist entry we opened in May — leveraged non-bank intermediaries holding concentrated, richly-valued US assets — reached two-of-three coherence this month. The trigger was the regulatory layer: the FSB's report on vulnerabilities in private credit, which describes a market that has grown to an estimated $1.5–2 trillion and, in its own words, has not yet been tested through a severe downturn. That is the corroboration our agents had been waiting for, and the signal is now fully flagged.

- The reflationary regime survived the ECB meeting. June's macro fulcrum was the 11 June Governing Council decision. We will not pretend to have known the precise calibration in advance, and the point of the regime framework is that we do not need to: whatever the exact move, the decision confirmed a central bank reacting to realised, energy-led inflation rather than to a forecast. Regime C stayed modal.

- Dollar-funding stress entered the watchlist. A persistent oil bid is a dollar bid. As energy-importing corporates rebuilt hedges and term-funded larger import bills, Microstructure Watcher began picking up widening in short-dated cross-currency basis for a cluster of non-US energy importers. It is early and one-layer; we are sharing it now, as we always do.

Three flagged signals

Signal #1 — Non-bank leverage and private-credit concentration: graduated to flagged

What the agent flagged: May's watchlist entry had a single coherence layer — Issuer Scout's dispersion across leveraged non-bank intermediaries, with Microstructure Watcher seeing funding-sensitivity widen in the same names. In June the regulatory layer arrived. Regulatory Crawler surfaced the FSB's private-credit report and the broader non-bank monitoring work, which together frame exactly the vulnerability our agents were measuring: leverage, liquidity mismatch, and concentration in a sector that the FSB notes now accounts for roughly half of global financial assets. That lifts the signal to two-of-three coherence and across our publication threshold.

Why it matters: This is the channel through which a market repricing becomes a forced-selling event. If leveraged non-banks holding concentrated, richly-valued assets are pushed to deleverage into a falling market, losses propagate back to banks through the financing and counterparty linkages the FSB highlights between private-credit funds and banks, insurers, and private-equity sponsors. In a reflationary regime with a higher-for-longer path now confirmed, that is the precondition worth flagging before it matures, not after.

Operationalised: For institutions with financing or counterparty exposure to leveraged non-banks and private-credit vehicles, this is the month to re-confirm collateral terms and to stress the second-round effect of an asset drawdown on those counterparties — not just the first-round mark on your own book. PortIQ users can run the non-bank deleveraging scenario against financing and prime-brokerage exposures.

Signal #2 — Commodity-financing dispersion: resolving into the energy shock

What the agent flagged: The commodity-financing cluster we have tracked since the spring continued to resolve in June. Of the five live names carried out of May, the dispersion signal on three has now compressed back toward the cohort, helped by the throughput-revenue side of a sustained energy bid. Two remain wide, and on those two the dispersion is now driven by funding cost rather than asset quality — the signature of higher rates rather than impaired books.

Why it matters: A sustained energy shock is double-edged for commodity financiers — higher throughput revenue, but larger drawn facilities and fatter funding needs. The fact that three names resolved while two re-widened on funding cost is the cleanest evidence yet that the binding constraint has shifted from the commodity to the cost of money. That is consistent with the macro read and tells us the cohort is now a rates story, not a credit story.

Operationalised: For the three resolved names, the cautious overlay can be lifted, with one flagged for follow-through on use of proceeds from its earlier capital raise. For the two live names, hold the overlay but reframe the re-test around funding-cost sensitivity rather than commodity-price sensitivity.

Signal #3 — Dollar-funding and cross-currency-basis stress: entering watchlist

What the agent flagged: As the oil bid persisted, Microstructure Watcher began aligning on a funding signal distinct from the leverage story: short-dated cross-currency basis widened for a cluster of non-US energy-importing corporates rebuilding hedges and term-funding larger import bills. Issuer Scout does not yet corroborate at the name level, so this is a one-layer, microstructure-only entry — but it is exactly the kind of funding-plumbing pressure a divergent policy path tends to surface first.

Why it matters: Dollar-funding stress is rarely the headline and almost always the transmission belt. When energy importers compete for the same dollars at once, the basis becomes the early warning for a broader short-dollar squeeze. We are watching whether the issuer layer corroborates; if it does, this graduates the way the non-bank signal did this month.

Operationalised: For treasuries with dollar liabilities funded in local currency, this is the month to re-check the cost and tenor of the cross-currency hedge and to map the rollover calendar against the basis, rather than assuming last quarter's funding cost holds.

Macro lens — the Macro Simulator's June read

End-June regime weights:

- Regime A — "Compressed vol, dispersing fundamentals": weight 0.27 (down from 0.30). The benign state keeps bleeding weight as the supply shock proves persistent rather than transitory; there is no longer a credible path back to compressed vol while energy stays bid.

- Regime B — "Coordinated repricing": weight 0.27 (up from 0.24). The increase is deliberate and specific: the graduated non-bank-leverage signal makes correlated, forced-deleveraging repricing the dominant propagation risk, and the weight reflects that channel moving from possible to flagged.

- Regime C — "Reflationary surprise": weight 0.38 (unchanged) and still the modal regime. The energy-led inflation impulse that lifted CPI through the spring did not reverse, and the ECB's 11 June decision confirmed policy reacting to a realised shock. The regime did not need to rise further this month; it needed to hold, and it held.

- Regime D — "Plumbing stress": weight 0.08 (unchanged). The payment-system signal that created this regime in May stayed contained in its two corridors and did not escalate. We keep the weight small and explicit rather than retiring it.

The composite read is "supply-shocked with correlated risk, now propagating through non-bank balance sheets." Where last month's discipline was re-staging reflation hedges, this month's is mapping the second-round channel: which counterparties would be forced to sell, into which markets, if the higher-for-longer path squeezes leveraged holders of richly-valued assets. The FSB's private-credit and non-bank work describes the same backdrop from the supervisory side, which is why we treat its publication as a coherence layer rather than as background reading.

Reader question of the month

"If oil is starting to stabilise, even at a high level, why keep the reflationary regime modal instead of fading it?" — Chief Risk Officer at a European asset manager

Because stabilising at a high level is not the same as reversing, and the regime is calibrated to the inflation impulse, not the oil tape. A price that holds near four-year highs keeps feeding the year-on-year comparison and keeps the policy reaction in place; it is the level, not last week's direction, that sustains the reflationary state. We would fade Regime C on a corroborated turn — oil rolling over and the policy path softening and our agents confirming — not on a single calmer week.

There is also an asymmetry worth naming. The cost of holding the regime one month too long is a slightly conservative book; the cost of fading it too early, into a confirmed higher-for-longer path, is being underhedged when the non-bank channel we just flagged starts to bind. Given that trade-off, holding at 0.38 is the disciplined choice.

What we are reading

- The FSB Report on Vulnerabilities in Private Credit (May 2026) — the central regulatory document behind this month's graduated signal, particularly its treatment of leverage, liquidity mismatch, and bank–non-bank interconnection in a market it describes as untested through a severe downturn.

- The FSB Global Monitoring Report on Non-Bank Financial Intermediation 2025 — essential context for the scale of the channel, including the finding that non-banks now represent roughly half of global financial assets.

- The forthcoming BIS Annual Economic Report — for its recurring work on energy-shock pass-through, the monetary-policy backdrop, and the rise of non-banks.

Coming in July

- 7 July — Private credit under a reflationary regime: a PortIQ scenario walkthrough.

- 14 July — Reading the cross-currency basis: a practitioner's guide to dollar-funding stress.

- 21 July — Did our flagged signals pay off? Backtesting watchlist graduations without fooling ourselves.

- 28 July — Risk Heartbeat #07.

— The DF Analytics Research team

Frequently asked questions

What does it mean that the non-bank-leverage signal "graduated"?

It moved from the watchlist to a fully flagged signal. We require two-of-three coherence across our agent layers — microstructure, issuer, and regulatory — before publishing a signal as flagged. The May entry had the microstructure and issuer layers; in June the regulatory layer appeared in the form of the FSB's private-credit and non-bank work, crossing the threshold.

Why is private credit specifically a concern now?

Because it has grown quickly — the FSB estimates the market at $1.5–2 trillion — while remaining untested through a severe downturn, and because its interconnections with banks, insurers, and private-equity sponsors are deepening. In a confirmed higher-for-longer rate environment, leverage and liquidity mismatch in that ecosystem are exactly the vulnerabilities that turn a repricing into forced selling.

Did the ECB's 11 June decision change the regime?

It confirmed it rather than changed it. Regime C was already modal going into the meeting, and the decision validated a central bank reacting to a realised, energy-led inflation shock rather than to a forecast. We treat the meeting as corroboration of the existing reflationary read, not as a new trigger.

What is the difference between Signal #1 and Signal #3?

Signal #1 is a leverage-and-concentration story — who is forced to sell if richly-valued assets reprice. Signal #3 is a funding-plumbing story — who is squeezed for dollars when energy importers compete for the same liquidity. They can interact, but they are measured by different agents and would graduate on different evidence.

How do you keep the reflationary regime from becoming a permanent call?

By tying it to corroborated evidence and publishing in both directions. Regime C holds while the inflation impulse and the policy reaction both persist; it falls when oil rolls over, the policy path softens, and our cross-asset agents confirm the turn. A regime that rises on corroboration falls on corroboration.

Related reading

- Risk Heartbeat #05 — May 2026 issue

- VaR vs. CVaR in stressed regimes: a 2008/2020 benchmark

- Time-series forecasting in finance: features, leakage, drift

External references

- FSB — Report on Vulnerabilities in Private Credit (May 2026)

- FSB — Global Monitoring Report on Non-Bank Financial Intermediation 2025

- BIS — Annual Economic Report

About the author — Research team — Deep Finance Analytics. Our Research team produces the agent-driven signal and quantitative analysis behind Risk Heartbeat and Aspects. See the Insights hub for the full archive, or book a discovery call to discuss this post with the team.