Risk Heartbeat #03 — March 2026 issue

Risk Heartbeat March 2026 — Financials signal priced in, commodity-financing dispersion graduates, EU AI Act clarifying note on agent documentation.

Welcome to issue #03 of Risk Heartbeat. March was the month in which two of the patterns we have been watching either resolved or graduated, and the regulatory perimeter for agent-driven systems came back into focus.

The format is the same: what changed, three flagged signals, one macro lens, reader question, what we are reading.

8-minute read · Updated 16 May 2026

Key takeaways

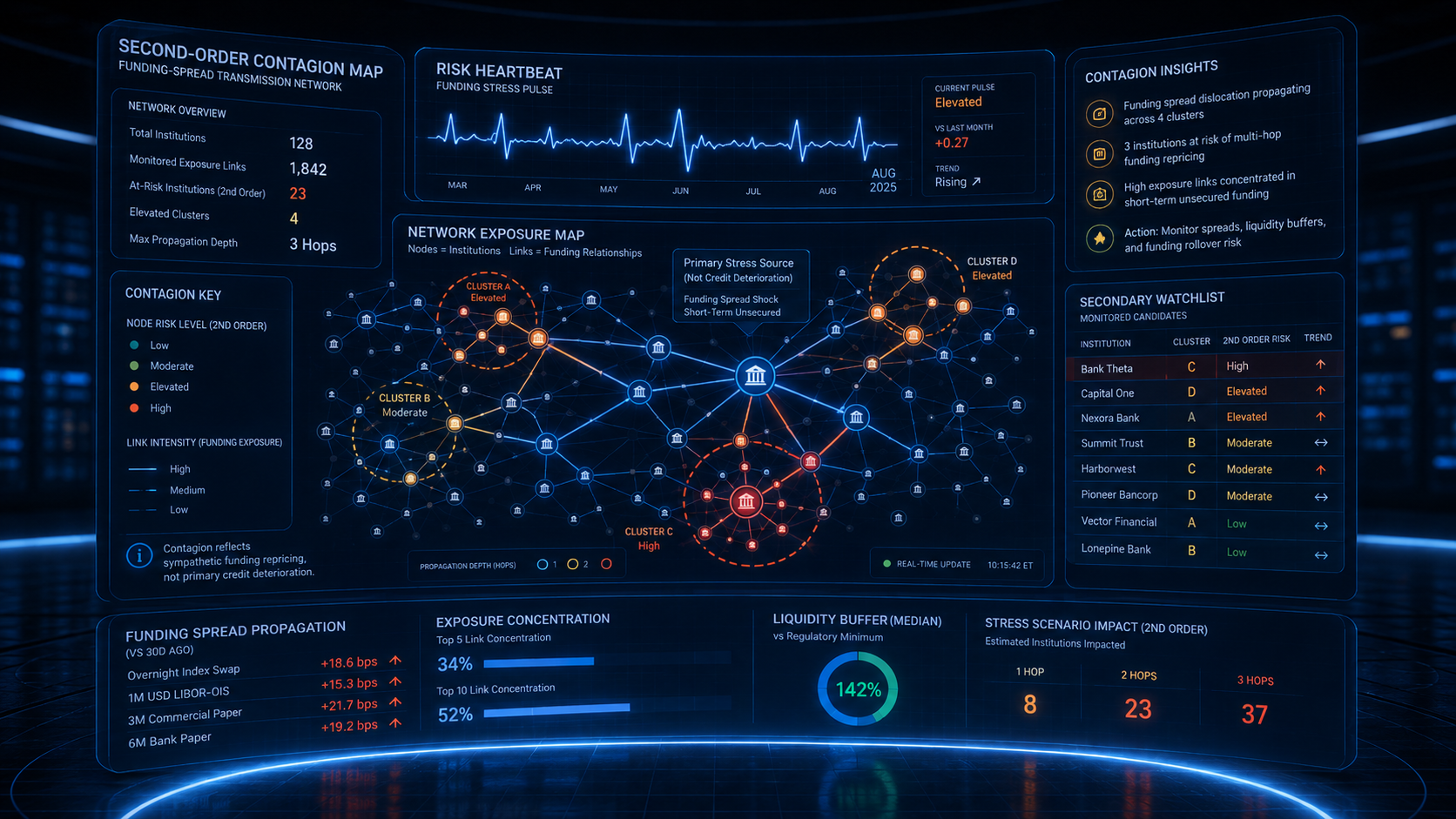

- The Financials liquidity signature priced in for the primary eight-name cluster; 11 second-order contagion candidates entered the watchlist.

- Commodity-financing dispersion graduated to a fully flagged signal across European and Middle Eastern banks with commodity-backed lending exposure.

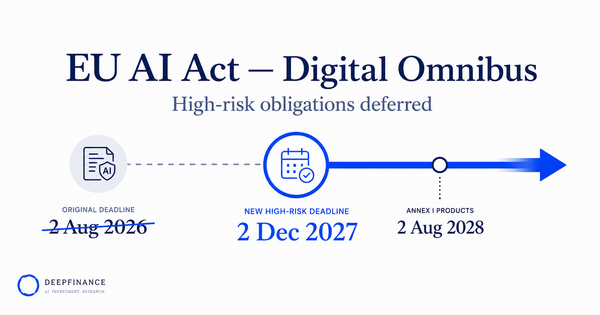

- With the EU AI Act's main high-risk obligations approaching their August 2026 application date, the documentation bar for agent-based systems is the regulatory item we are watching most closely.

- Regime A weight eased to 0.45 as the Financials thesis partially resolved; Regime B (coordinated repricing) regained probability with second-order contagion risk.

What changed in March 2026

Three headlines:

- The Financials liquidity signature priced in. Funding spreads for the eight-name cluster we have been tracking widened by a further 18bps on senior unsecured and 31bps on AT1, and two of the eight names exhibited measurable price discontinuities mid-month. The signal is no longer informative on a forward-looking basis for this cluster — it has played out. We are pivoting attention to the second-order names that may now reprice on contagion.

- Commodity-financing dispersion graduated from watchlist to fully flagged signal. The coherence we mentioned in February strengthened across the language layer, the microstructure layer, and the regulatory layer. New Aspects mid-cycle note coming in April.

- The AI Act documentation bar moved up the agenda. With the main high-risk obligations approaching their 2 August 2026 application date, the question of what supervisors will expect to see when they audit agent-based AI components is now a planning question, not a future one. We are continuing to align our internal templates to the Act's lifetime-documentation obligation.

Three flagged signals

Signal #1 — Financials: second-order contagion candidates

What the agent flagged: Following the funding-spread widening in the primary eight-name cluster, Issuer Scout flagged a new set of 11 European banks whose funding metrics moved in sympathy without an obvious idiosyncratic trigger. This is the textbook contagion signature: institutions whose fundamentals are largely fine but whose funding cost adjusts on the actions of correlated peers.

Why it matters: Contagion candidates are different from primary signals. They are not flagged because something is wrong inside the institution; they are flagged because the funding environment around them changed. The remedies are different too — these institutions cannot fix their fundamentals in response, only the funding environment around them can change.

What we would do with it: For portfolios with material European bank exposure, the second-order cluster is where active management can still add value this quarter. Run an Epsilon screen over the contagion candidates, look for the names whose funding move is the most disproportionate to their fundamentals, and you have the natural set of opportunistic adds. Do not treat the cluster as homogeneous.

Signal #2 — Commodity-financing dispersion: graduated

What the agent flagged: Coherent language shifts across eight European and Middle Eastern banks with material commodity-financing exposure. Funding terms on trade-finance and commodity-backed lending programmes have tightened — measurable in syndicated loan pricing — even as headline credit metrics for the affected institutions remain unchanged.

Why it matters: This is the same pattern that played out in European Financials a quarter earlier: tightening of funding for a specific lending franchise before the institution-level metrics catch up. Two of the eight names are exposed at the franchise level above 15% of total lending; the rest are smaller but coherent.

What we would do with it: Add the cluster to internal watchlists. The April mid-cycle Aspects note will go deeper into the pattern with the gated edition naming the institutions.

Signal #3 — EU AI Act: the documentation bar for agents

What we are watching: As the Act's main high-risk obligations approach their August 2026 application date, the practical question for firms running agent-based AI is what their documentation will need to show under audit. The Act's lifetime-documentation obligation (Article 11, Annex IV) requires technical documentation to be drawn up before deployment and kept up to date throughout the system's life — and in our reading, agent-based components raise the bar for what that means in practice.

Why it matters: For an agent-based component, keeping documentation current over its life means being able to produce, at any moment:

- The agent's source perimeter, with timestamped change history.

- The agent's prompt, system-message, and tool-definition configuration, version-controlled.

- The agent's rate-limit and cost-cap configuration, with the rationale.

- The agent's challenger and disagreement log.

- The agent's incident history.

This is exactly the structure of the template we published last week, which we built to meet the Act's lifetime-documentation obligation. Firms whose agent documentation is built as a periodic deliverable will likely need to restructure toward a continuous, runtime-generated pattern.

What we would do with it: Audit your agent-based components against the five bullets above. Items that cannot be produced in one click are the items most likely to attract supervisory attention in the next dialogue cycle.

Macro lens — the Macro Simulator's March read

End-March regime weights:

- Regime A — "Compressed vol, dispersing fundamentals": weight 0.45 (down from 0.51). The Financials repricing partially resolved the dispersion thesis.

- Regime B — "Coordinated repricing": weight 0.24 (up from 0.19). Some Financials contagion risk has re-elevated this regime.

- Regime C — "Reflationary surprise": weight 0.31 (effectively flat).

The shift in March is small but worth noting: as the dispersion regime partially resolves through repricing, the coordinated-repricing regime regains some probability. The composite implication for portfolios is to slightly reduce the residual-aware tilt that has paid off this quarter and to increase the weight on coordinated-shock hedges.

Reader question of the month

"You said in the LLM-MRM template that you generate the documentation continuously from runtime state. What happens when the foundation model provider releases a new version mid-quarter — does the documentation just update overnight without a validation cycle?" — Head of Validation at a large UK asset manager

This is the right question to ask. The short answer: no, the documentation does not silently update for a model-version change. The longer answer is in how we treat provider-version changes.

A new foundation-model version is treated as a controlled change. Specifically:

- The new version is pinned in a non-production environment.

- The full labelled validation set is re-run on the new version.

- The challenger comparison is re-run on the new version.

- If performance metrics remain within acceptable thresholds, the change is approved through the configuration governance process (Principle 9 from the governance post).

- The version pin is updated in production, and the documentation reflects the new pin from that point.

- If performance metrics deviate beyond threshold, the change is held back and an exception is raised.

This means the continuous-documentation pattern does not mean "documentation drifts with the world." It means "the documentation reflects the current authorised state, which is itself version-controlled." The provider-version change is a documented event with a sign-off, not a silent update.

If you want to walk through the change-management pattern in detail, the discovery call is the right setting.

What we are reading

- Commentary on the EU AI Act's high-risk obligations ahead of the August 2026 application date — useful for any firm finalising its readiness plan for agent-based systems.

- A buy-side research note on contagion risk in European bank funding — directionally consistent with the second-order pattern we flagged this month.

- The Aspects Q1 download data and the upcoming April mid-cycle note on commodity-financing.

Coming in April

- 7 Apr — Inside the agent stack: Issuer Scout, Microstructure Watcher, Regulatory Crawler.

- 14 Apr — Two-tier agents: why we run cheap scouts before deep ones.

- 21 Apr — Industry Risk Intelligence Platform: the free tier that earns paid usage.

- 28 Apr — Risk Heartbeat #04, plus mid-cycle Aspects note on commodity-financing.

— The DF Analytics Research team

Frequently asked questions

What does 'priced in' mean in Risk Heartbeat?

A signal that has translated into measurable price or funding-cost change. The information value of the signal for forward-looking decisions has been consumed; attention pivots to second-order effects.

What is second-order contagion?

Funding cost adjustments at institutions whose fundamentals are largely fine but whose funding environment changed because of related peers. Different remedy than primary signals — these institutions cannot fix their fundamentals in response.

How does Risk Heartbeat handle watchlist signals?

Watchlist signals are signals at the 'interesting' stage that do not yet satisfy the two-of-three coherence rule. They are published transparently so readers can see signals before they harden, and so we can be held to account when one does not mature.

What is the watchlist hit rate?

As of end-Q1 2026, roughly 55% of watchlist entries mature into fully flagged signals within two quarters. Around 30% dissolve. The remaining 15% are still open. We publish the resolution of every watchlist signal in the issue in which the resolution occurs.

Related reading

- Risk Heartbeat #02 — February 2026 issue

- MRM documentation template for LLM-based agents

- Inside the agent stack: Issuer Scout, Microstructure Watcher, Regulatory Crawler

External references

About the author — Research team — Deep Finance Analytics. Our Research team produces the agent-driven signal and quantitative analysis behind Risk Heartbeat and Aspects. See the Insights hub for the full archive, or book a discovery call to discuss this post with the team.