AI-native risk intelligence: 5 tests for 2026

Five concrete tests that separate AI-native risk intelligence from legacy risk reporting with an LLM bolted on. A buyer's working definition.

The word "AI-native" is now on so many product pages it has started to lose shape. We have seen it applied to spreadsheets with a chatbot on the side, to risk systems whose only AI component is a sentiment label on news headlines, and — most generously — to platforms built from the ground up to make machine learning, agents, and quantitative engines first-class citizens of the architecture.

If you are evaluating tooling in 2026 — or defending a procurement decision to a board — you need a precise definition. This post offers one: **five tests** that separate a genuinely AI-native risk intelligence stack from a legacy system with AI stickers on top.

We will not name competitors. The point of these tests is not to win an argument; it is to give buyers a checklist they can hand to a vendor and read the answers.

- "AI-native" is now overused; the five tests in this post separate genuine architecture from LLM stickers on a legacy stack.

- The tests cover narrative-to-math workflow, agents as a layer, explainability as substrate, built-in model risk management, and deployment portability.

- A platform that cannot demonstrate all five in a 60-minute call is not AI-native, regardless of marketing language.

- Cost is managed by architectural choices: two-tier agents, retrieval grounding, and feature/inference caching — not by capping usage.

Why this matters now

Two things have changed in the last twenty-four months.

First, the underlying models got useful. Large language models can now reliably extract structured signal from filings, transcripts, and unstructured documents — the kind of work that used to require a team of analysts and three days. Quantitative ML models for time-series forecasting and anomaly detection are no longer research curiosities; they sit inside production trading and risk systems at every major institution we talk to.

Second, the regulators noticed. The EU AI Act, SR 11-7 updates, and the rolling guidance from DIFC, FCA, and BaFin all now contemplate AI/ML inside risk decisions. "Governed by default" used to be a sales line; in 2026 it is becoming an audit prerequisite.

The result: every vendor wants to claim AI-native. But the architectures underneath are wildly different — and the difference shows up in cost, in audit defensibility, in the speed at which you can answer a board question, and in whether you can extend the platform without rewriting it.

The five tests

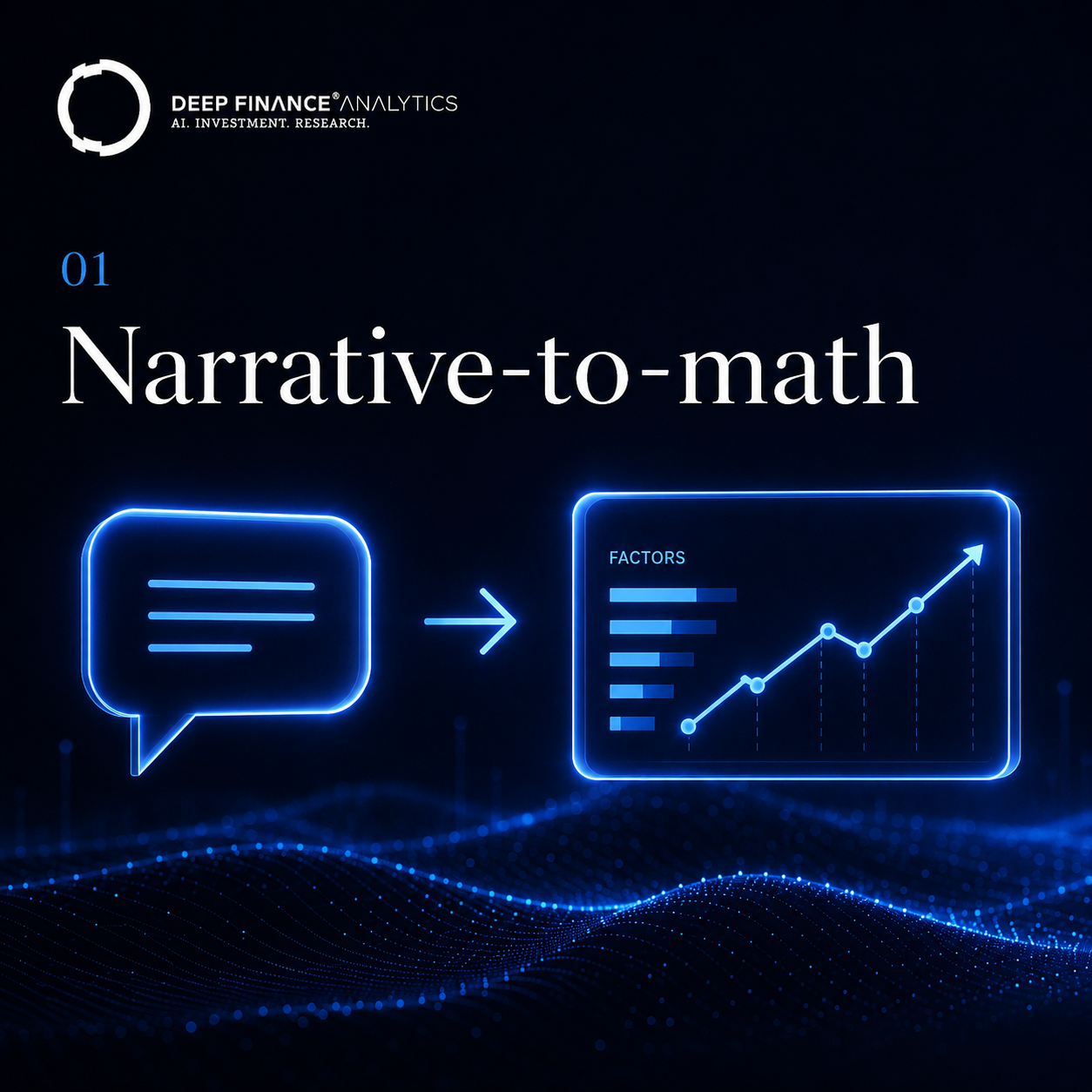

Test 1 — Narrative-to-math is a first-class workflow, not a chatbot

Many vendors have added an LLM chat sidebar. A user can ask "what is my VaR?" and get a sentence. That is convenient, but it is not narrative-to-math.

The native architecture lets a user describe a scenario in plain language — "Tech selloff with credit widening and EM contagion" — and have the system translate that into quantified factor shocks across the entire portfolio, with a P&L impact and a hedging proposal. Then it lets the user iterate on the scenario in language, not in spreadsheets.

The test: can the system run a scenario you describe in a sentence, and produce auditable factor shocks, expected P&L, and a proposed action — without a quant manually wiring up the inputs?

Test 2 — Agents are part of the stack, not a feature

In a legacy system, agents are something a customer might add via API. In a native system, agents are a layer of the architecture. At Deep Finance Analytics we run three: Issuer Scout (filings, news, alternative data), Microstructure Watcher (liquidity and order-flow anomalies), and Regulatory Crawler (rule changes, enforcement, jurisdictional signals). Each one runs 24/7 against a shared feature store and feeds a single "Risk Heartbeat" stream of prioritised signals.

The test: does the platform have autonomous agents that surface risk signals into the same data layer the quant engines consume, with rate limits, hallucination guards, and human-escalation triggers configured by default?

If agents only exist as a sales demo, or only run against one data source, the architecture is not native.

Test 3 — Explainability and audit trails are the substrate

This is where the legacy-vs-native split becomes most expensive to fix retroactively. In a native architecture every output — every signal, every proposal, every score — carries an evidence chain: which features were used, which model version produced it, when it was last validated, and what the confidence interval looks like.

In a non-native system, explainability is bolted on. Engineers write reports that try to reconstruct a decision after the fact. This is slow, fragile, and the first thing a regulator probes.

The test: can you produce, in less than 60 seconds, the full lineage of any single number on the screen — back to source data, with model version, confidence, and validation status — without engineering effort?

Test 4 — Model risk management is built in, not a workpaper

SR 11-7, the EU AI Act, and most national frameworks now require model registries, challenger models, drift monitoring, and a documented validation cadence. In a native stack these are not Excel workpapers maintained by a separate MRM team; they are platform features. Drift monitors run continuously. The model registry is the system of record. Challenger models are spun up automatically alongside production models.

The test: does the system ship with a model registry, automated drift monitoring, challenger comparisons, and scheduled validation reports — or are those activities still handled outside the tool?

Test 5 — Deployment optionality without rewrites

A native stack is portable. The same engines that power a managed SaaS deployment should run inside a customer-managed VPC, an on-prem cluster, or a sovereign cloud — with no architectural difference. If a vendor needs to do a "different version" for on-prem, the architecture is leaky.

The test: can the platform deploy as managed SaaS, customer-managed Private VPC, and on-prem / sovereign cloud from a single codebase, with the same governance and observability features in each mode?

What the tests rule out

This is what the five tests fail to rule out — deliberately:

- Open source vs. proprietary models. Both can be AI-native. The test is the architecture, not the model provenance.

- Cloud vs. on-prem. AI-native is not synonymous with managed SaaS. Some of our own customers run the full stack in a private VPC with customer-managed keys.

- Generative vs. classical ML. We use both. The architecture is what matters, not whether the system has a chat box.

What the tests do rule out:

- A risk reporting tool with an LLM chat sidebar bolted on.

- A scenario engine where the only AI involvement is sentiment scoring of news headlines.

- A platform where governance is delivered as Word documents rather than as platform features.

- A vendor whose on-prem deployment is materially different software from their SaaS.

A short note on cost

There is a reasonable concern that AI-native means expensive. In a poorly architected system it does. Token costs run away, generative calls happen where retrieval would have worked, and inference repeats because nothing is cached.

A native stack handles this in three ways:

- Two-tier agents. Cheap "scout" agents do the triage; deeper, more expensive agents only run on validated signals.

- Retrieval-grounded generation. Generative calls are minimised in favour of retrieval against curated, version-controlled knowledge.

- Feature and inference caching. The same query does not pay twice.

These are architectural choices, not features you can switch on later.

What to do on Monday morning

If you are evaluating a vendor in this space, send them the five tests. Specifically:

- Show me a narrative-to-math scenario, end-to-end, on representative data.

- Show me the agent layer and what data it touches.

- Click any number on the screen and produce the lineage in under 60 seconds.

- Open the model registry and show me a drift report from yesterday.

- Walk me through how the same engine deploys to SaaS, VPC, and on-prem.

If the vendor cannot show all five in a 60-minute call, the platform is not AI-native — whatever the homepage says.

Where DF Analytics fits

For full disclosure: this post is written by the team behind a platform that scores all five tests. PortIQ does the narrative-to-math; Issuer Scout, Microstructure Watcher, and Regulatory Crawler are the agent layer; every output in PortIQ carries an evidence chain; the model registry, drift monitors, and challenger comparisons ship by default; and all of it runs in managed SaaS, Private VPC, or on-prem from one codebase.

That is the architecture we wish had existed when we were sitting on the other side of these procurement decisions. It is the architecture we build now.

If you want to put the five tests to PortIQ yourself, request an evaluation — we will set up a dedicated environment with your asset class and walk through each one with our engineering team.

Frequently asked questions

What is AI-native risk intelligence?

AI-native risk intelligence is a risk platform whose architecture treats machine learning, autonomous agents, and quantitative engines as first-class layers — not as features bolted onto a legacy reporting tool. It supports narrative-to-math workflows, explainable evidence chains, and continuous model governance by default.

How is AI-native different from a chatbot on top of a risk system?

A chatbot translates a question into a query against an existing report. An AI-native system translates a plain-language scenario into quantified factor shocks, P&L impact, and a hedging proposal — with the entire path back to source data auditable in one click.

Does AI-native mean cloud-only?

No. An AI-native platform should deploy as managed SaaS, customer-managed Private VPC, or on-prem / sovereign cloud from a single codebase, with the same governance features in each mode.

How do regulators view AI-native risk platforms?

Regulators (EU AI Act, SR 11-7, DIFC DFSA, FCA, BaFin) increasingly expect built-in model registries, drift monitoring, challenger models, and continuous documentation. AI-native architectures meet these expectations natively; bolted-on AI struggles to.

What does an evaluation of an AI-native platform look like?

Apply the five tests in this post end-to-end on representative data: scenario engine, agent layer, evidence chain, model registry, and deployment portability. A genuine platform demonstrates all five in a single working session.