Risk Heartbeat #02 — February 2026 issue

Welcome to issue #02 of Risk Heartbeat. February is a short month and a busy one — three of the four signals we covered in January moved meaningfully, and one materially new signal entered our watchlist.

The format is the same as last month: what changed, three flagged signals, one macro lens, the reader question, what we are reading.

7-minute read · Updated 16 May 2026

Key takeaways

- The Financials liquidity signature graduated from leading to coincident — the four-signature composite crossed the coincident threshold in mid-February.

- EM sovereign liquidity mean-reverted in the basket we flagged in January, with bid-ask spreads contracting to within 8bps of trailing average.

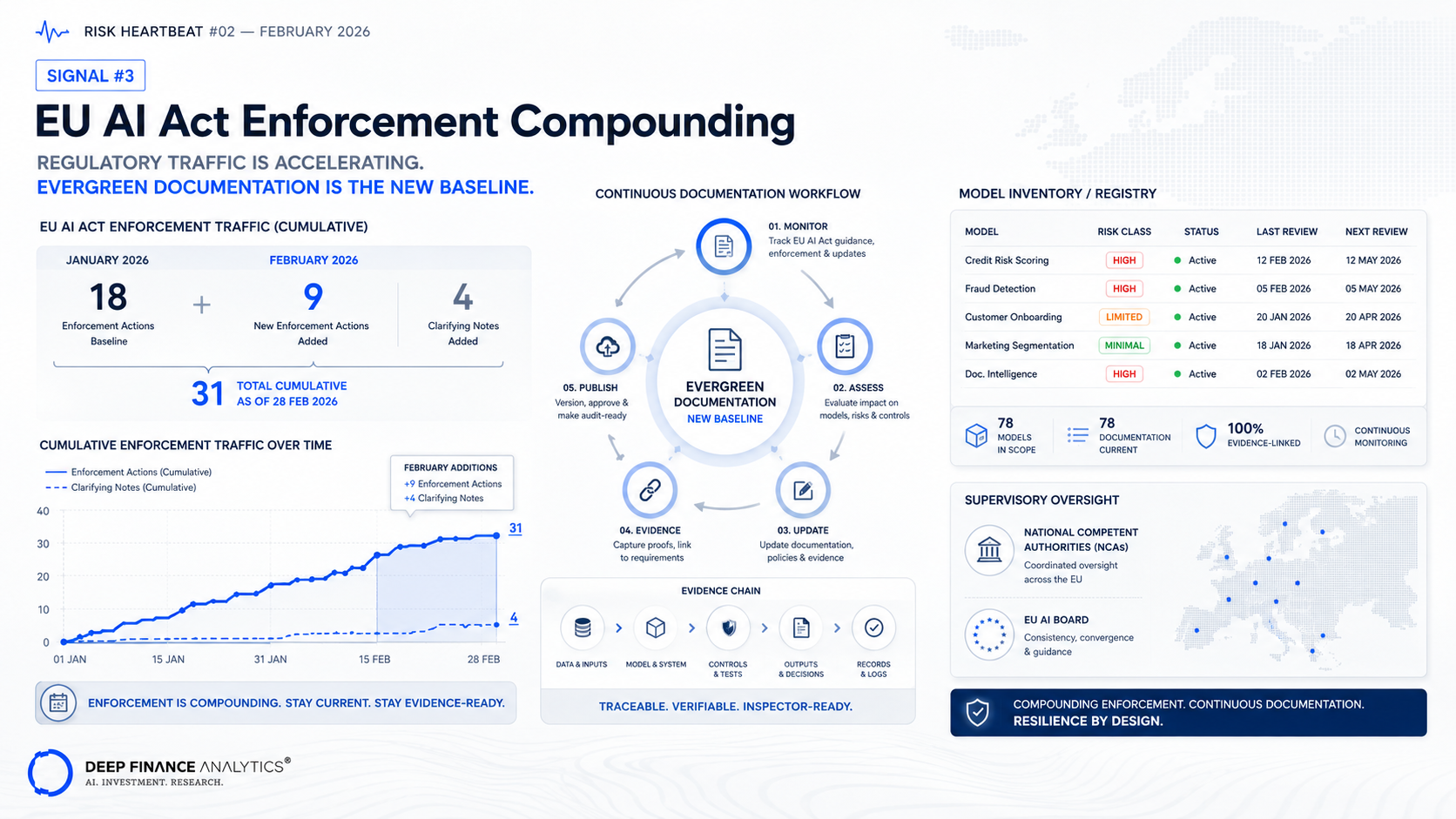

- EU AI Act regulatory traffic compounded — nine new regulatory and supervisory items and four pieces of clarifying commentary flagged by Regulatory Crawler this month, cumulative trend unambiguous.

- Regime A (compressed vol, dispersing fundamentals) remains the modal regime at 0.51 weight, but coordinated-repricing risk re-elevated marginally.

What changed in February 2026

Three headlines:

- The Financials liquidity signature became coincident, not leading. The drawn-revolver dispersion we wrote about in Aspects Q1 has now translated into measurable funding-spread widening for the specific issuer cluster we flagged. The signal has graduated from "watch" to "act-or-explain-why-not."

- EM sovereign liquidity stabilised in the basket we flagged in January. Bid-ask spreads contracted to within 8bps of the trailing average, and order book depth recovered. This is what mean-reversion looks like.

- EU AI Act regulatory traffic compounded. Nine new regulatory and supervisory items and four pieces of clarifying commentary flagged by Regulatory Crawler this month, on top of the six and two we flagged in January. The cumulative trend is no longer ambiguous.

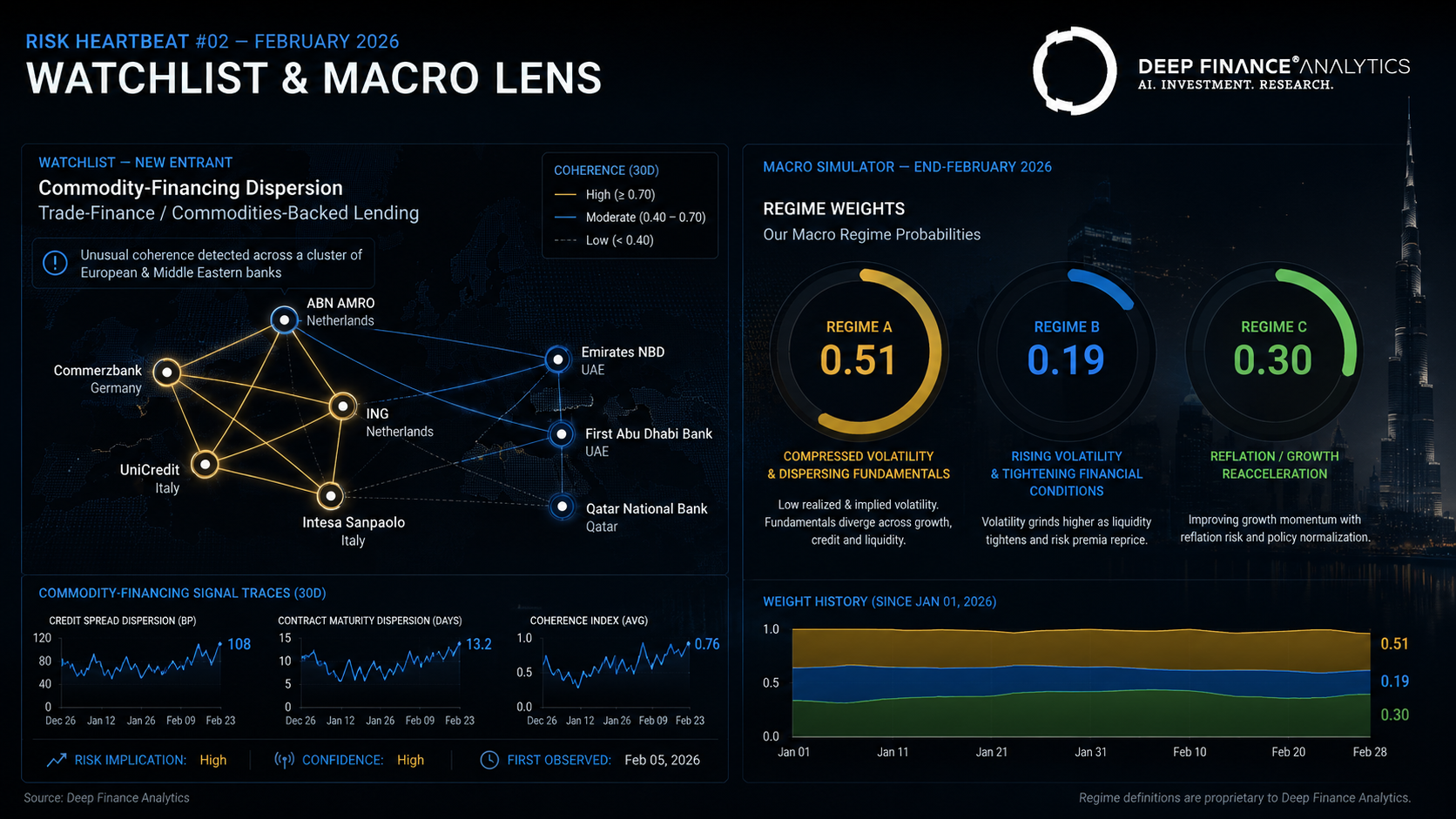

And one new entrant: commodity-financing dispersion in the trade-finance / commodities-backed-lending space, which Issuer Scout began flagging in the second half of the month.

Three flagged signals

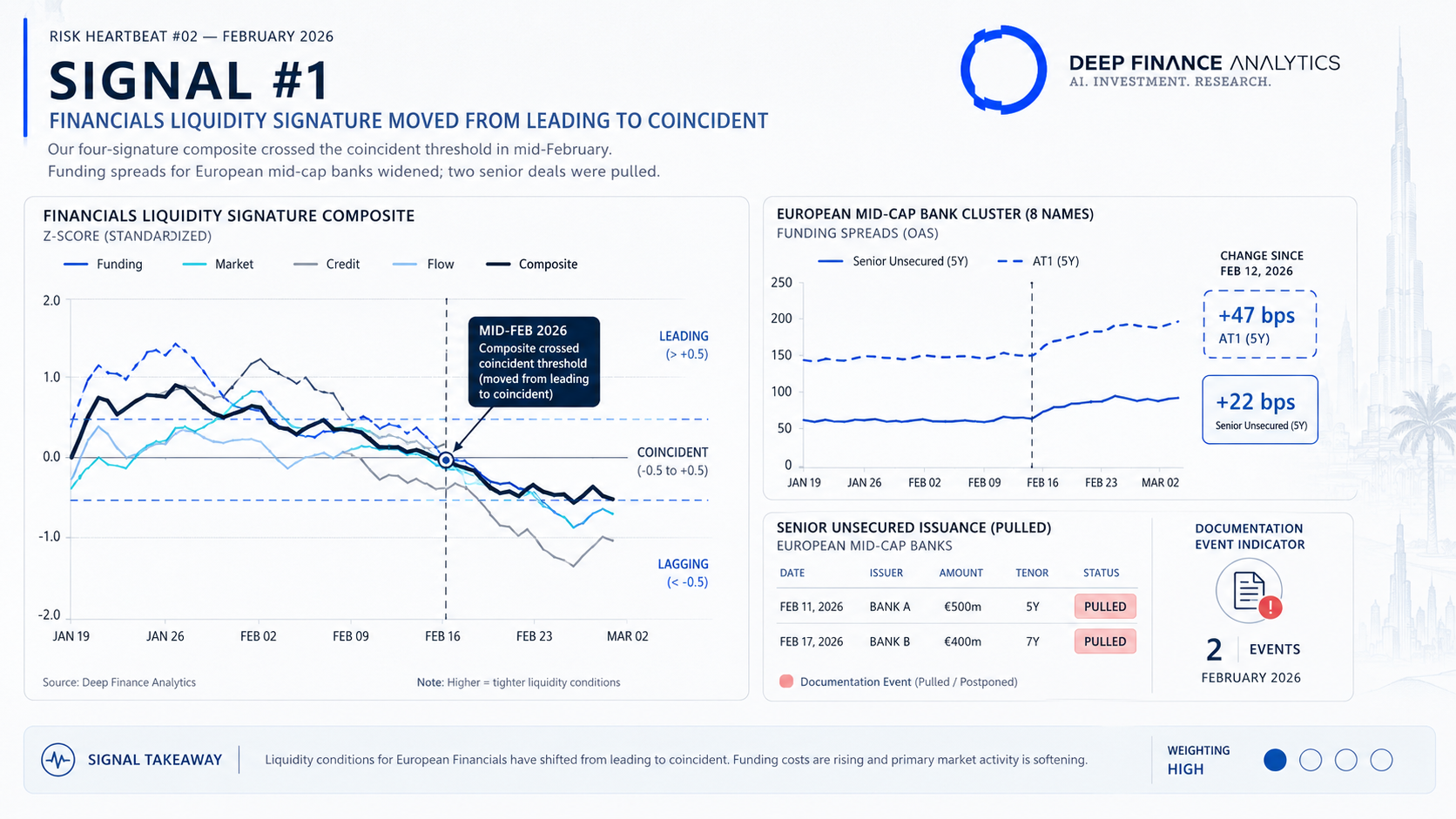

Signal #1 — Financials: from leading to coincident

What the agent flagged: Funding spreads for the eight-name European mid-cap bank cluster we flagged in Aspects Q1 widened by an average of 22bps across senior unsecured and 47bps across AT1. Two of the eight names also saw senior issuance pulled at advanced stages of marketing.

Why it matters: The four-signature composite (drawn-revolver dispersion, sentiment compression, microstructure withdrawal, regulatory traffic) crossed our coincident threshold in mid-February. The signal is no longer purely anticipatory; the funding stress is on the screen.

What we would do with it: If you have material exposure to the cluster and have not yet executed the pre-staged hedges discussed in Aspects, the cost of delay is now meaningful. The composite score crossing the coincident threshold is also a documentation event — it should be recorded in your risk-committee minutes with the action taken, even if the action is "we have chosen to hold."

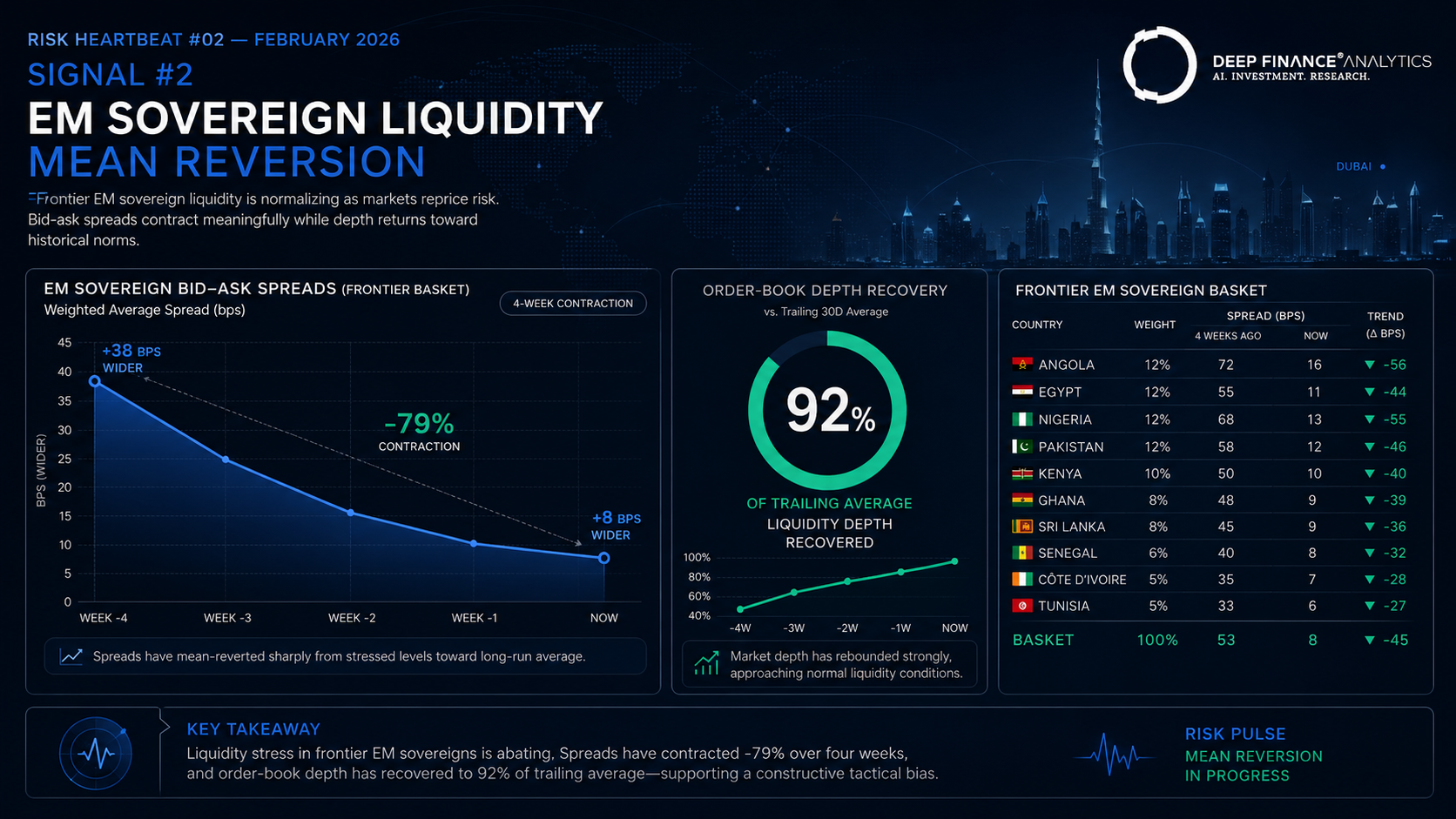

Signal #2 — EM sovereigns: mean reversion

What the agent flagged: The basket of frontier EM sovereigns we flagged in January saw bid-ask spreads contract from a peak +38bps wider to +8bps wider over four weeks. Order book depth recovered to 92% of the trailing average.

Why it matters: Liquidity withdrawal that does not translate into a price discontinuity within roughly 60 days typically mean-reverts. This is the favourable resolution of the January signal.

What we would do with it: Reduce the conservatism of the liquidation-window assumption for these names back toward the standard. Update the watchlist documentation; the action is "watch released" rather than "watch removed."

Signal #3 — EU AI Act: compounding signal

What the agent flagged: Nine regulatory and supervisory items and four pieces of clarifying commentary in February. The clarifying commentary increasingly touches on the cadence and depth of model documentation — consistent with the Act's lifetime-documentation obligation (Article 11, Annex IV), under which documentation is expected to be kept current rather than fixed at validation cycles.

Why it matters: The cumulative regulatory traffic over two months is now consistent enough to inform planning. Internal MRM teams should treat continuous documentation as the new baseline, and budget capacity accordingly. The expectation that documentation is an event has become an expectation that it is a process.

What we would do with it: If you are still treating AI/ML model documentation as a quarterly or annual deliverable, this is a budget conversation rather than a methodology one. Our March posts on the EU AI Act readiness checklist and the LLM-MRM template are designed to help.

Entering the watchlist — commodity-financing dispersion

This is a new entrant rather than a fully formed signal. Issuer Scout began flagging unusual coherence in the language around commodity-backed lending exposure across a small cluster of European and Middle Eastern banks. The signal is at the "interesting" stage; we will know by next month whether the coherence persists and translates into balance-sheet or microstructure signatures.

We flag this here to be transparent about our process: the watchlist exists publicly so that readers can see signals before they harden, and so that we can be held to account when one does not mature.

Macro lens — the Macro Simulator's February read

End-February regime weights:

- Regime A — "Compressed vol, dispersing fundamentals": weight 0.51 (up from 0.48). The Financials development supports this further.

- Regime B — "Coordinated repricing": weight 0.19 (down from 0.22). The EM mean-reversion eased this regime.

- Regime C — "Reflationary surprise": weight 0.30 (flat).

The compressed-vol-with-dispersing-fundamentals regime is now our highest-weighted regime by a clear margin. Portfolios constructed for "low vol everywhere" are most vulnerable in this regime; the natural defence is shifting risk budget toward residual-aware constructions and toward conditional hedges.

Reader question of the month

"You mentioned in the factor models post that the agent layer can trigger regime-aware re-estimation of factor loadings. How often does that actually happen in practice, and what is the audit trail?" — Head of MRM at a Swiss asset manager

Good and specific question. In our deployed PortIQ instances, the regime-aware re-estimation triggers fire on average 3–5 times per year per asset class. Some asset classes are quieter (developed-market sovereign debt typically sees 1–2 per year); some are noisier (emerging-market equities can see 6–8). The triggers themselves are calibrated per asset class; we do not run a one-size-fits-all threshold.

The audit trail captures, for every trigger event:

- The agent signals that crossed the composite threshold (each signal with its evidence chain).

- The factor model version before and after the re-estimation.

- The change in factor loadings and the change in the portfolio-level risk view.

- A human-in-the-loop sign-off if the re-estimation crosses a configured magnitude.

The point of the sign-off threshold is that small, frequent re-estimations are routine; large re-estimations require a human risk officer to approve before the new loadings are committed to the live risk view. This is a governance pattern we recommend across all agent-driven model adaptation.

What we are reading

- The Bank of England's February consultation paper on third-party AI services in financial services — useful framework, particularly for firms running externally hosted AI infrastructure.

- A research note from a major US asset manager on residual concentration in the AI-infrastructure sector — independent confirmation of the cluster pattern we flagged in January, from a different methodology.

- The Aspects Q1 download data: thank you for the strong response; we will publish the gated edition data appendix as a separate technical note in March.

Coming in March

- 3 Mar — Governance by default: nine principles for AI in institutional finance.

- 10 Mar — EU AI Act readiness checklist for asset managers (2026).

- 17 Mar — MRM documentation for LLM-based agents: a template you can use.

- 24 Mar — Risk Heartbeat #03.

— The DF Analytics Research team

Frequently asked questions

What does a coincident liquidity signature mean?

A signal that has moved from forward-looking (predicting future stress) to contemporary — the funding stress is now on the screen in measurable funding-spread widening, not just in early-warning indicators.

Why does EM sovereign liquidity mean revert?

Liquidity withdrawal that does not translate into a price discontinuity within roughly 60 days typically mean-reverts. The withdrawal was a precursor; the absence of a price gap allowed normalisation.

What is EU AI Act regulatory traffic compounding?

A monthly count, flagged by Regulatory Crawler, of regulatory and supervisory items and clarifying commentary that is no longer ambiguous as a trend. Cumulative regulatory traffic over two months is consistent enough to inform internal planning.

How does the regime-weight model work?

The Macro Simulator maintains a small set of named macro regimes and assigns probability weights based on observable state variables and current agent-detected signal coherence. Weights are updated monthly and surfaced as part of Risk Heartbeat.

Related reading

- Risk Heartbeat #01 — January 2026 issue

- Aspects Q1 — Financials: liquidity-stress signatures

- Factor models in 2026: what to keep, what to fix

External references

- Bank of England — third-party AI services consultation

- EBA — bank funding supervision

- BIS — global liquidity indicators

About the author — Research team — Deep Finance Analytics. Our Research team produces the agent-driven signal and quantitative analysis behind Risk Heartbeat and Aspects. See the Insights hub for the full archive, or book a discovery call to discuss this post with the team.