Risk Heartbeat #04 — April 2026 issue

Risk Heartbeat April 2026 — commodity-financing dispersion graduates, second-order Financials contagion partially resolves, new payment-system signal.

Welcome to issue #04 of Risk Heartbeat. April was a month of resolution on some patterns we have been tracking since the start of the year, graduation on others, and one genuinely new signal.

The format is unchanged: what changed, three flagged signals, one macro lens, reader question, what we are reading.

8-minute read · Updated 16 May 2026

Key takeaways

- Commodity-financing dispersion graduated to a fully flagged signal; mid-cycle Aspects note published.

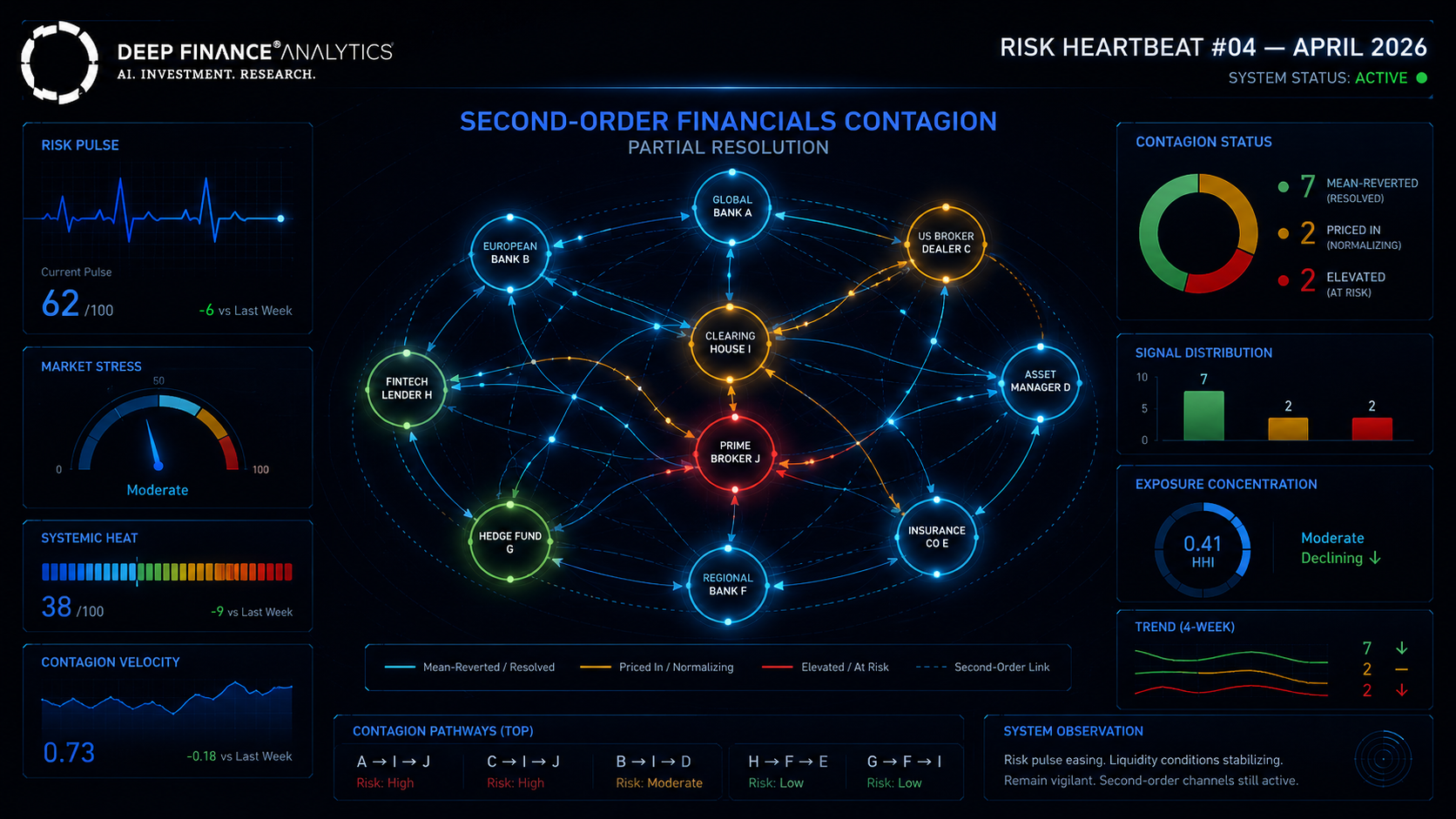

- Of 11 second-order Financials contagion candidates flagged in March, 7 mean-reverted, 2 priced in, 2 remain elevated.

- Cross-border payment-system stress entered the watchlist — early microstructure signal in two specific corridors, not yet at two-of-three coherence.

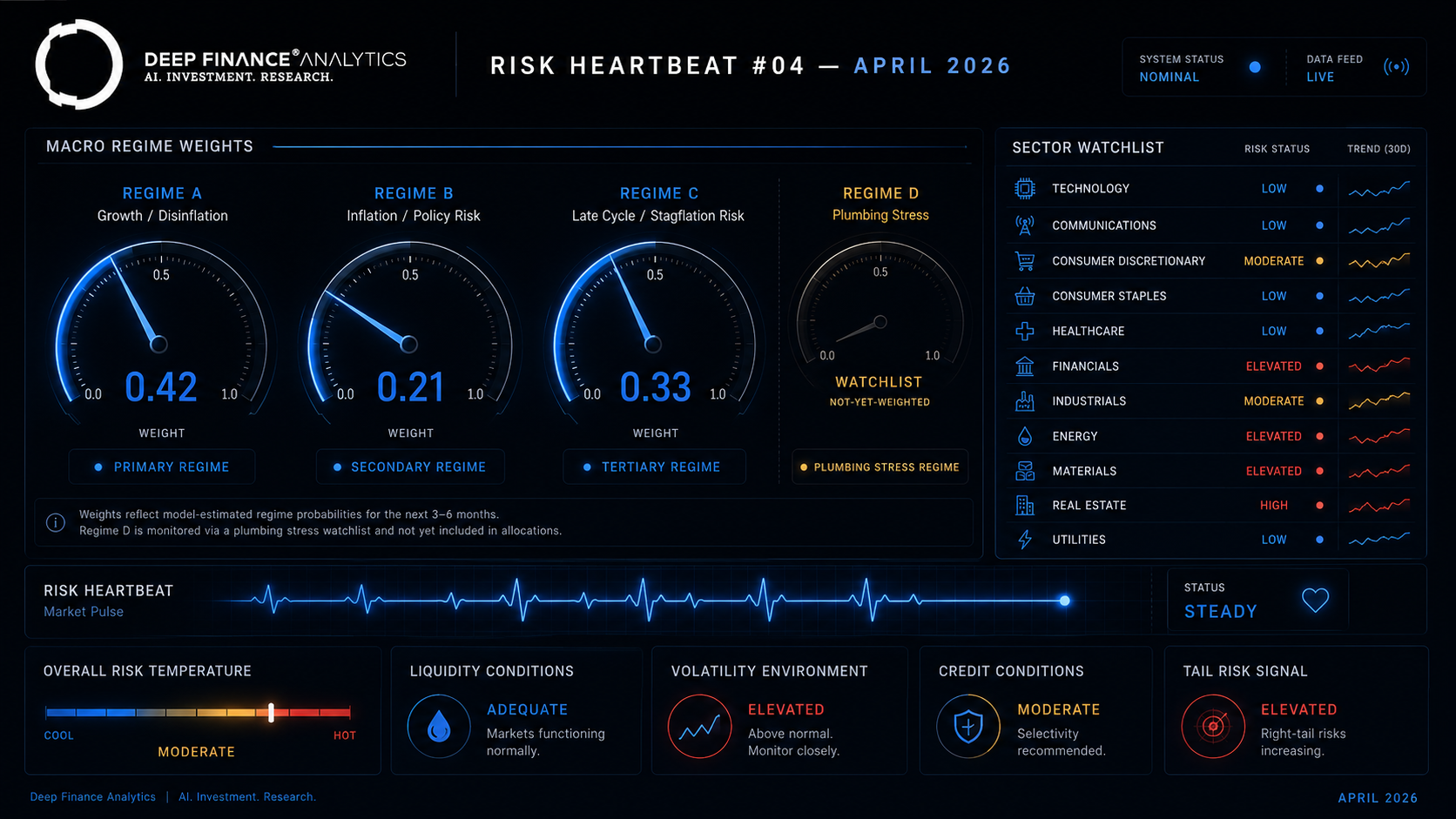

- Regime A weight eased to 0.42; Regime C (reflationary surprise) rose slightly to 0.33 on April inflation prints.

What changed in April 2026

Three headlines:

- Commodity-financing dispersion fully graduated with a mid-cycle Aspects note published this week. The cluster of eight European and Middle Eastern banks now shows microstructure withdrawal and regulatory traffic on top of the language and balance-sheet signatures we flagged earlier.

- Second-order Financials contagion partially resolved. Of the 11-name contagion candidate cluster we flagged in March, 7 mean-reverted, 2 priced in, and 2 remain on watch. This is a healthier outcome than we expected.

- Cross-border payment-system stress entered the watchlist. Microstructure Watcher began flagging unusual liquidity behaviour in a small number of cross-border instant-payment corridors. It is early; we are sharing it transparently rather than waiting for it to mature.

Three flagged signals

Signal #1 — Commodity-financing dispersion: full Aspects mid-cycle

What the agent flagged: The eight-name commodity-financing cluster (six European banks, two Middle Eastern banks) now exhibits coherent signal across all four signatures we track: drawn-revolver dispersion analogue, language compression on commodity-finance exposures, microstructure withdrawal in bank capital instruments, and elevated supervisory communication traffic.

Why it matters: This is the same composite pattern that played out in the broader European Financials sector across Q1. The mechanism is different — commodity financing has its own underwriting and liquidity dynamics — but the early-warning structure is analogous, and it is replicating about one quarter behind.

What we would do with it: Read the mid-cycle Aspects note (published today on the Insights hub). The gated edition names the institutions and walks through a worked PortIQ scenario on a representative portfolio.

Signal #2 — Second-order Financials contagion: partial resolution

What the agent flagged: Of the 11 second-order contagion candidates flagged in March, 7 saw funding-spread mean reversion, 2 priced in (single-name re-rating events), and 2 remain elevated without resolution either way.

Why it matters: The 7-out-of-11 mean reversion is a meaningful resolution of the broader Financials thesis. It suggests the primary cluster's repricing did not propagate as widely as it might have — likely because the supervisory dialogue and bank-by-bank funding adjustments contained the contagion.

What we would do with it: For exposures in the 7 mean-reverting names, the cautious overlay can be released. For the 2 priced-in names, the loss has crystallised. For the 2 still-elevated names, document the continued watch — the second-order story is not closed.

Signal #3 — Cross-border payment-system stress: entering watchlist

What the agent flagged: Microstructure Watcher began flagging unusual liquidity behaviour in a small number of cross-border instant-payment corridors — specifically widening of intra-day liquidity premia and concentration in a smaller number of clearing institutions per corridor. The pattern is concentrated in two specific corridors and is week-old at the time of writing.

Why it matters: Payment-system stress is rare but consequential. The signal is early and we do not yet have coherence across the other agent layers; Issuer Scout has not flagged anything, and Regulatory Crawler has not yet seen related supervisory communications. The two-of-three coherence rule means this would not be a published Risk Heartbeat signal under normal circumstances — but the magnitude on the microstructure layer is large enough that we are sharing it transparently rather than waiting.

What we would do with it: For institutions with material exposure to clearing institutions in the affected corridors, ask the question of treasury teams now: "do we know which counterparties we depend on in these corridors, and what is our backup?" The probability the signal matures is uncertain; the cost of asking the question is small.

Macro lens — the Macro Simulator's April read

End-April regime weights:

- Regime A — "Compressed vol, dispersing fundamentals": weight 0.42 (down from 0.45). The partial resolution of the Financials story and the second-order mean reversion eased this regime.

- Regime B — "Coordinated repricing": weight 0.21 (down from 0.24). The mean reversion eased coordinated-shock risk as well.

- Regime C — "Reflationary surprise": weight 0.33 (up from 0.31). Modestly higher as inflation data in two major economies surprised to the upside in April.

- Watch for regime D — "Plumbing stress": not yet weighted, but the cross-border payment signal could mature into a new regime if other signal types align. We will create a regime explicitly if it does.

The compressed-vol regime is still the modal regime, but its weight has fallen meaningfully. The composite implication for portfolios is to start trimming residual-aware tilts that have paid off this quarter and to begin pre-staging reflationary scenarios for the back half of the year.

Reader question of the month

"You publish the watchlist signals before they mature. If a watchlist signal doesn't mature, do you ever publish the dis-confirmation?" — Head of Risk at a US asset manager

Yes — and we appreciate the question because it is a discipline worth being explicit about.

We commit to publishing the resolution of every watchlist signal in the Risk Heartbeat issue in which the resolution occurs. If a watchlist signal matures into a fully flagged signal, we say so. If it dissolves without maturing, we say so equally clearly. Both are useful information.

We also keep a public log on the Insights hub of every watchlist entry and its resolution status. The discipline matters because the value of publishing early signals depends on transparency about how often they materialise. A watchlist that only ever surfaces hits is a watchlist with selection bias.

The historical hit rate, as of end-Q1 2026, is roughly 55% for watchlist entries maturing into fully flagged signals within two quarters. Around 30% dissolve without maturing. The remaining 15% are still open. We will publish a fuller methodology note on this in May.

What we are reading

- The mid-cycle Aspects note on commodity-financing dispersion — published today.

- A BIS working paper on payment-system resilience in cross-border corridors — directionally relevant to the new watchlist entry.

- Ongoing supervisory commentary on AI-driven model risk in financial services — consistent with the direction our own LLM-MRM template takes.

Coming in May

- 5 May — VaR vs. CVaR in stressed regimes: a benchmark on 2008 and 2020.

- 12 May — Time-series forecasting at the engine level: features, leakage, drift.

- 19 May — Quantitative Engines: the eight APIs and when to use which.

- 26 May — Risk Heartbeat #05.

— The DF Analytics Research team

Frequently asked questions

Why did 7 of 11 second-order Financials candidates mean revert?

Mean reversion suggests the primary cluster's repricing did not propagate as widely as it might have. Supervisory dialogue and bank-by-bank funding adjustments likely contained the contagion.

What is cross-border payment-system stress?

Unusual liquidity behaviour in cross-border instant-payment corridors — intra-day liquidity premia widening, concentration in a smaller number of clearing institutions. Rare but consequential if it matures.

Why publish a watchlist signal before it matures?

Transparency. Publishing early lets readers see signals before they harden and lets us be held accountable when one does not mature. We track the watchlist hit rate publicly (~55% maturation rate within two quarters as of Q1 2026).

How are macro regime weights updated?

Monthly. Each Macro Simulator regime has a probability weight determined by observable state variables and current agent coherence. The weights feed portfolio construction discipline — for example, avoiding accidental single-regime optimisation.

Related reading

- Risk Heartbeat #03 — March 2026 issue

- Industry Risk Intelligence Platform: free sector lens

- Two-tier agents: the cost and quality argument

External references

About the author — Research team — Deep Finance Analytics. Our Research team produces the agent-driven signal and quantitative analysis behind Risk Heartbeat and Aspects. See the Insights hub for the full archive, or book a discovery call to discuss this post with the team.