Risk Heartbeat #01 — January 2026 issue

Risk Heartbeat January 2026 — three agent-flagged signals on idiosyncratic dispersion, EM sovereign liquidity, EU AI Act enforcement, plus macro lens.

Welcome to the first edition of Risk Heartbeat — the monthly drumbeat from Deep Finance Analytics. Each issue compresses what our agents (Issuer Scout, Microstructure Watcher, Regulatory Crawler) and the Risk Brain saw during the month into something you can read in ten minutes.

The format is consistent and will be the same every month:

- What changed — the headline.

- Three flagged signals — one from each agent, with evidence.

- One macro lens — what the Macro Simulator is pricing.

- Reader question of the month.

- What we are reading.

Let us begin.

8-minute read · Updated 27 January 2026

Key takeaways

- Idiosyncratic dispersion in mid-cap tech rose sharply while index volatility stayed compressed — a classic precursor pattern.

- EM sovereign liquidity withdrew without a yield move in two specific issuers, flagged by Microstructure Watcher.

- EU AI Act enforcement traffic was the highest monthly count since the Act came into force — six actions and two clarifying notes.

- Macro Simulator regime weights now favour "compressed vol, dispersing fundamentals" — idiosyncratic risk pays in this regime.

What changed in January 2026

Three things stood out across the data we monitor:

- Idiosyncratic dispersion rose sharply in mid-cap tech, while the headline index volatility stayed compressed. The gap between index-implied vol and our issuer-level dispersion measure widened to its highest level since Q4 2022. This is the pattern that historically precedes single-name shocks; it does not always precede them, but the conditional probability has shifted meaningfully.

- Credit spreads on lower-quality issuers stopped tightening for the first time in nine weeks. Index-level credit looks calm; the cross-section is starting to fan out.

- Regulatory action picked up in EU AI Act implementation. Six enforcement actions and two clarifying notes hit our Regulatory Crawler this month — the highest monthly count since the Act came into force.

We treat these as observations, not forecasts. Each one is unpacked below.

Three flagged signals

Signal #1 — Issuer Scout: AI-infrastructure mid-caps

What the agent flagged: A cluster of 14 mid-cap AI-infrastructure issuers showed simultaneous filings activity around capex revisions, alongside a measurable shift in sell-side language. Twelve of the fourteen revised capex guidance downward in the same earnings window; sentiment in the accompanying transcripts moved from "scaling" to "discipline" in the same period.

Why it matters: This is not yet a price story — index-level performance is in line. But the narrative coherence across a cluster of names is the kind of signal that historically precedes a re-rating event. Our Epsilon engine ticked up the cluster's idiosyncratic risk score by 0.27 (on a 0–1 scale) over the month.

What we would do with it: This is a "watch and tighten" signal, not a "trade now" signal. For a portfolio with concentrated exposure, we would shorten the liquidity window we assume for these names and pre-stage the hedging options.

Signal #2 — Microstructure Watcher: EM sovereign liquidity

What the agent flagged: Bid-ask spreads on a basket of frontier EM sovereigns widened by an average of 38 basis points in the second half of January, with no corresponding move in headline yields. Order book depth dropped 22% week-over-week in two specific issuers.

Why it matters: Liquidity withdrawal without a yield move is a classic precursor to a price discontinuity. It is also the signal that is most often invisible to a factor-model-only view of the world; you have to be in the order book to see it.

What we would do with it: Flag the affected positions in any liquidity stress overlay. Review the assumed liquidation window in any internal mandate that touches these names.

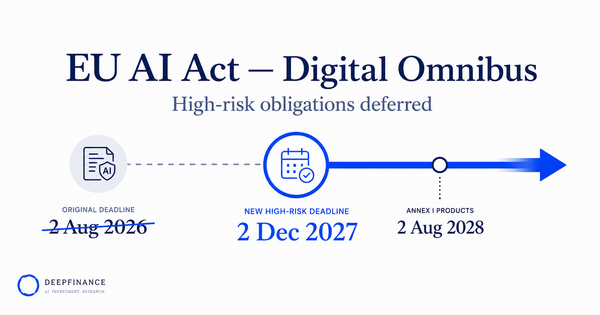

Signal #3 — Regulatory Crawler: EU AI Act enforcement

What the agent flagged: Six enforcement actions and two clarifying notes against AI-driven financial services. The clarifying notes specifically address model documentation completeness — the bar appears to be higher than many firms have assumed for risk and analytics applications.

Why it matters: The market priced the EU AI Act as a one-time compliance event when it came into force. Our read of the January actions is that the standing compliance burden — particularly around documentation cadence and challenger-model evidence — is materially higher than the initial market read suggested.

What we would do with it: If you have not run a documentation completeness check against the latest guidance, this is the month. We are publishing a 2026 readiness checklist in March — meanwhile, the Industry & Regulation pillar on Insights will track this closely.

Macro lens — the Macro Simulator's January read

We use the Macro Simulator (one of our free-tier tools) to maintain a small set of named regimes and check, monthly, where they sit relative to our agent signals. As of end-January 2026 the three live regimes are:

- Regime A — "Compressed vol, dispersing fundamentals." Probability weight 0.48 (up from 0.42 last month). This is the regime in which idiosyncratic risk pays off and broad index hedges do not. Most of January's signals support this regime.

- Regime B — "Coordinated repricing." Probability weight 0.22 (down from 0.28). A broad rates-and-credit shock together. Lower likelihood than last month but still material; the EM liquidity signal nudged this up slightly.

- Regime C — "Reflationary surprise." Probability weight 0.30 (flat). Inflation prints in major economies surprise to the upside, central banks slow rate cuts.

The point of the regime weighting is not to forecast which one occurs. It is to make sure portfolios are not optimised for a single regime by accident.

Reader question of the month

"How does Epsilon decide which idiosyncratic flags are worth surfacing? We see hundreds of small anomalies in our own data every week." — CRO at a European insurer

Good question, and the honest answer is layered.

Epsilon scores each issuer on three dimensions: (1) a model-based anomaly score from the time-series engine, (2) a narrative coherence score from the LLM-based Risk Brain, and (3) a microstructure score from Microstructure Watcher. The surfaced flags are those where at least two of the three scores are elevated and the resulting composite is in the top decile of issuers in the universe for that week.

The point of the two-of-three rule is to suppress single-signal noise — the price anomaly that turns out to be a settlement effect, the narrative shift that turns out to be a wording change, the liquidity dip that turns out to be a quarter-end book-cleaning. Coherence across signal types is the filter that keeps the flag rate to roughly 0.4% of the investable universe per week — a number small enough for a human IC to read.

If you have a question for the next Risk Heartbeat, reply to the newsletter or email us; we answer one per month.

What we are reading

A short list, with our usual disclaimer that we link out without endorsing:

- The Bank for International Settlements' January working paper on agentic AI in financial services — useful framing of the governance perimeter, mostly aligned with our own thinking.

- A new buy-side research piece on realised dispersion vs. implied vol in US equities. Confirms the divergence our agents picked up this month from a different angle.

- The DIFC's updated guidance on outsourced AI services — relevant if you are a regulated entity using third-party AI tooling (which is most of you).

We will link each of these on the Insights hub.

Coming in February

February's Tuesdays:

- 3 Feb — Opening of the Aspects franchise with Q1 Financials: liquidity-stress signatures.

- 10 Feb — Epsilon: scoring issuer-specific risk the way IC wants to see it.

- 17 Feb — Factor models in 2026: where they still help and where they hide risk.

- 24 Feb — Risk Heartbeat #02.

Thank you for reading the first issue. If you want this in your inbox each month, subscribe at the bottom of any Insights page.

— The DF Analytics Research team

Frequently asked questions

What is the Risk Heartbeat?

Risk Heartbeat is DF Analytics' monthly research note. It compresses what our agents (Issuer Scout, Microstructure Watcher, Regulatory Crawler) and the Macro Simulator saw during the month into a short, structured read.

How are Risk Heartbeat signals selected?

Signals must satisfy a two-of-three coherence rule — at least two of the three agents (out of Issuer Scout, Microstructure Watcher, Regulatory Crawler) must flag the same entity within a defined window. The composite must also rank in the top decile.

Are the Risk Heartbeat signals investment advice?

No. The signals are observations of agent-detected coherence across data layers, published for context and discussion. They are not recommendations to buy, sell, or hold any specific security.

How do I follow the Risk Heartbeat monthly?

Subscribe at the bottom of any DF Analytics Insights page. The newsletter is delivered once a month and the back catalogue lives on the Insights hub.